GET IN TOUCH

- Please wait...

Not too long ago, a friend of mine shared a post on Facebook from Euromonitor International titled “Top 5 Fastest Growing Key Emerging Economies in 2014”. I was happy (and definitely not surprised) to see that Bangladesh had made 4th position on that list. What I was disappointed to see was a wary “for now” attached in parenthesis following the subheading “Bangladesh in 4th Position”. What struck me as a bit unfair was that there were other developing countries on the list which had their own share of risks. For instance, one of these countries faced significant external risks due to the continued reduction of quantitative easing in the United States. I did not find such cautionary phrases tagged with their outlook. I felt people insist on tagging our country with unstable politics, frequent strikes, and bureaucratic corruption – but isn’t it time we look at the brighter side of the economy which has helped us make the “Next-11” list of global investment banks Goldman Sachs?

When we look at the Medium-term to Long-term economic outlook, it should not surprise anyone that Bangladesh would make such lists. Nor that Bangladesh has the potential to maintain its position in these rankings. A closer look at the fundamentals which bring our trademark “above-6%” GDP growth should make it clear that our strengths far outweigh our challenges.

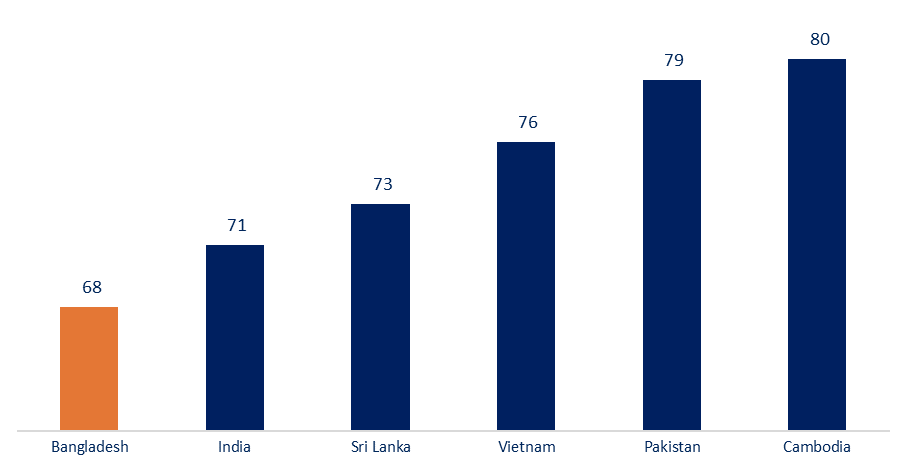

Bangladesh exhibits a relatively high population growth rate of 1.2%. Our 160mn population is characterized by a median age of 23 – meaning we have a large and youthful labor base. The wage rate is lower than most similar economies: implying we hold a critical edge in low labor costs. One might argue that the recent minimum wage hike at the end of 2013 has eliminated our strength. But a comparison between Bangladesh and some of its peers (Figure 1) below reveals that we hold the edge despite the increase in the minimum wage.

Figure 1: Monthly Minimum Wage Comparison

In spite of relatively lower wages, consumer demand has continued to rise: a 12% Compounded Annual Growth Rate (CAGR) of Per Capita GDP for the last ten years speaks for itself. Thus the economy is equipped with a large base of human resources at competitive wage levels, which will simultaneously drive the consumption of the economy.

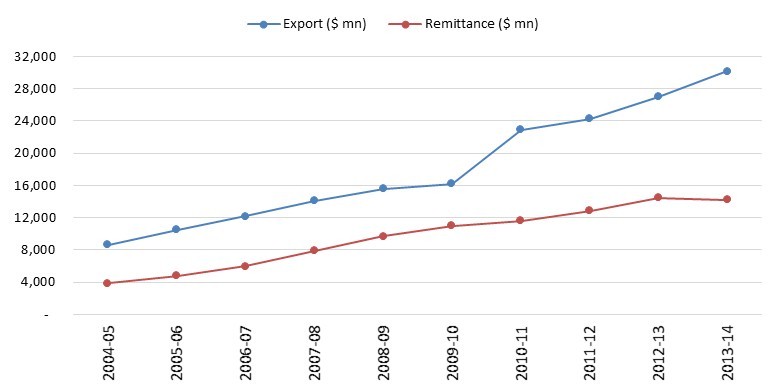

Exports And Remittance Have Long Led The Way

The “Twin-engines,” as I termed them in one of my previous posts, have long been the strongest drivers of our economy. Together, they brought in approximately USD 44 bn last fiscal year (over one-third of our GDP).

Figure 2: Bangladesh Exports and Remittance – Consistent growth over the years

As everyone knows, RMG consists of about 80% of our exports. Low labor costs and international quality products have helped us become the second largest RMG exporter after China. Furthermore, with RMG orders shifting from China to Bangladesh, export is well placed to continue its regular double-digit growth.

Figure 2 also makes it clear why we have been among the top ten highest remittance receivers for several years. It can be pointed out that in the last 37 months, we have had only 2 months where monthly remittance flow was less than USD 1bn (Source: Bangladesh Bank). However, we cannot close our eyes to the fact that remittance has taken a hit in the just-concluded fiscal year due mainly to a drop in net manpower export. Problems related to the legal status of Bangladeshi migrant laborers in Saudi Arabia, the United Arab Emirates, and Kuwait were the main factors behind the drop in manpower exports in 2013-14.

To revive growth in remittance, the government has taken various policies to export manpower to countries such as South Africa and Malaysia. Bangladesh has also started to export female workers to Hong Kong and Qatar. The effects of these initiatives can already be felt – remittance has returned to positive growth trajectories since February 2014 (after 6 consecutive months of negative growth) including a record-high USD 1.49 in July 2014 (21% growth compared to July of the previous year).

Agriculture has long ridden on the country’s large base of labor and has produced annual growth rates of about 4%-5% for much of the last ten years. The constraint of outdated technology and reduction in cultivable land has therefore not deterred an increase in productivity. Given the gradual transfer of technology, crop diversification, and introduction of higher-yielding seeds, agriculture has the potential of maintaining (and even increase) its current share of our GDP.

In recent times, the central bank has been quite successful in maintaining price stability in Bangladesh. For much of the last two years, Bangladesh Bank has managed to keep inflation at around its target of 7.5%. Over the years, it has become rigorous in restricting credit flow to unproductive sectors and thereby keeping inflation in check. And this year, with inflation at around 7%, it is again well on course to meet its inflation target.

Our central bank is also very adept at dealing with adversity. Take the example of the depreciation of the Taka in 2010-11. After enjoying remarkable stability between 2008 and 2010, our currency hit an alarmingly depreciating path in FY 2010-11. Bangladesh Bank, much to its credit, reacted with sound stabilization policies, including a hike in the lending rate.

In FY 2013-14, the exchange market was flooded with foreign currency due to a fall in imports and a steady inflow of exports earnings and remittances. To prevent the currency from appreciating sharply (which would hurt export and remittance), the central bank has initiated a commendable policy of removing excess liquidity from the market. As a result, the Taka, as everyone knows has been stable at around BDT 77-78 for the best part of the last two years.

It must also be noted that the central bank has not sacrificed its target for output or GDP growth to meet its primary objective of ensuring price stability. We have, after all, managed over 6% GDP growth for around a decade now. Therefore, from a monetary management perspective, we are definitely in good hands.

The Fiscal Side Does Not Look Too Bad Either

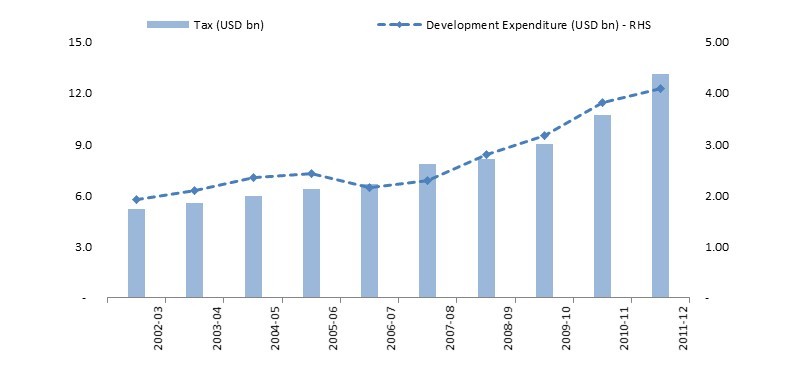

Revenue collection has increased at a CAGR of 11% for the last 10 years (Source: Bangladesh Bank). While a skeptic may point out that we have sometimes fallen short of our tax collection targets, one must remember that double-digit growth in revenue collection is not a feat to be overlooked. Consistent growth in tax collection has resulted in rising development expenditure. With growing development expenditure in recent years, substantial progress has been made in mitigating infrastructural inadequacies in power and transportation.

Figure 3: Bangladesh Tax Collection and Development Expenditure

Over the last 10 years, Bangladesh has generally maintained a current account surplus (barring infrequent and temporary deficits). Control in imports and the rise of export and remittance have helped bring about this favorable external position. Additionally, external debt to GDP dropped from 26.8% in 2007-08 to 20.8% at the end of FY 2012, which is lower than the emerging and developing market average of 24.5% (Source: The World Bank). Low external debt along with current account surplus and foreign exchange reserves of USD 22 bn (adequate for seven months of import payments) is indicative of a strong external position. This trend is likely to prevail in the future since the country is mostly dependent on domestic financing to cover its budget deficit.

I am certain I have left out many more of our economy’s strengths. These are just to name a few. But the whole point is to highlight the fact that associating Bangladesh with clichés such as “politically unstable” does not really capture the essence of our country or our macro-economy. One can always argue about our challenges and risks – addressing them is definitely of utmost importance. But perhaps the real picture of Bangladesh can be seen through these macroeconomic fundamentals, which have and will continue to hold the key to “The Bangladesh Growth Story.”

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights