GET IN TOUCH

- Please wait...

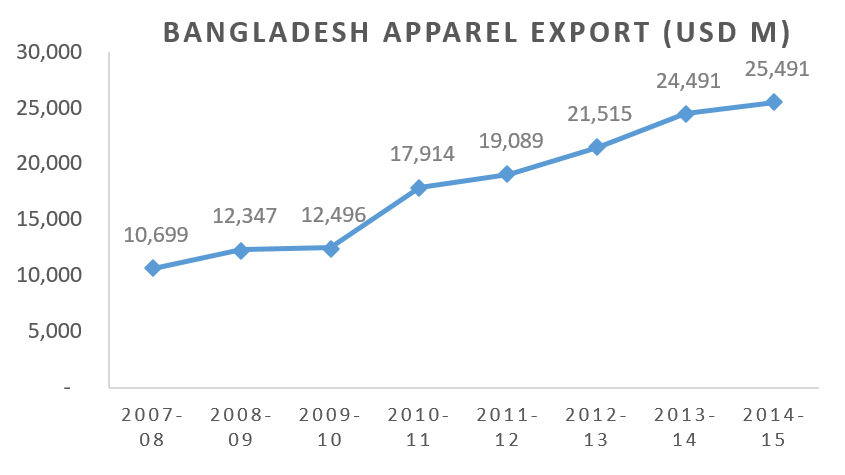

Bangladesh’s apparel sector has presented itself as a matured contributor to the country’s export and growth, contributing to 81% of the country’s export (USD25.4 Billion FY14-15) and employing a 4.2 million workforce. The sector’s meteoric rise in the global apparel market from the early 90s onwards has been augmented by inexpensive labor, favorable government policies, and preferential trade agreements. Bangladesh currently sits as the second-largest player in the market after China with a growing export forecast. While the sector has remarkable achievements over the last two decades, with changing dynamics in the global market and economy, apparel manufacturers and policymakers can ill afford to rest on their laurels.

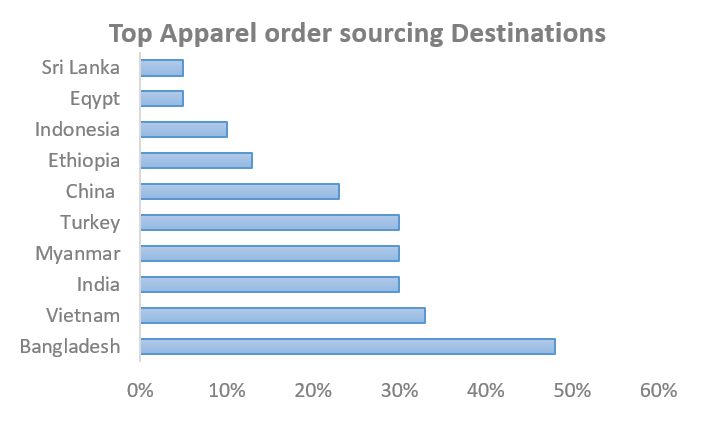

Bangladesh has been experiencing benefits of shifting orders from China since 2010, as the latter suffered from higher labor wages and rising overheads costs. China also consciously adopted a strategy of moving towards the manufacture of higher-margin products as opposed to apparel. This propelled Bangladesh as the second-largest apparel manufacturer. McKinsey, in their study on the apparel market in 2012, clearly pinpointed Bangladesh as the biggest beneficiary as most Chief Procurement Officers (CPOs) of major clothing brands identified Bangladesh as the most popular sourcing destination.

Over the last three years, several different players have emerged including Myanmar, which returned to the mainstream on the back of recent political reforms. Others are also offering competitive costing with the likes of Cambodia and Vietnam leading the way. The biggest long-term threat for Bangladesh is some of the Sub-Saharan African nations with Ethiopia posing as the major potential challenges. According to the latest Mckinsey report on the apparel sector published in 2015, Bangladesh still retains the preferred position for apparel sourcing but is closely followed by Vietnam, India, and Myanmar. Ethiopia became the first African country to make it to the list.

Sub-Saharan countries like Ethiopia enjoy a number of benefits through– preferential trade agreements (GSP to USA and EU), cheap labor (lower than Bangladesh), surplus electricity, cheap land price, preferential investment terms, and proximity to EU and USA. In the next decade, countries like Ethiopia can pose a major challenge in the low-value segment of the apparel market.

Despite sporadic political turmoil within the country, first in early 2014 and then in January 2015, Bangladesh’s apparel sector has maintained its steady growth, which is remarkable. In the international arena, several economic and political factors have been weighing against Bangladesh’s apparel sector growth.

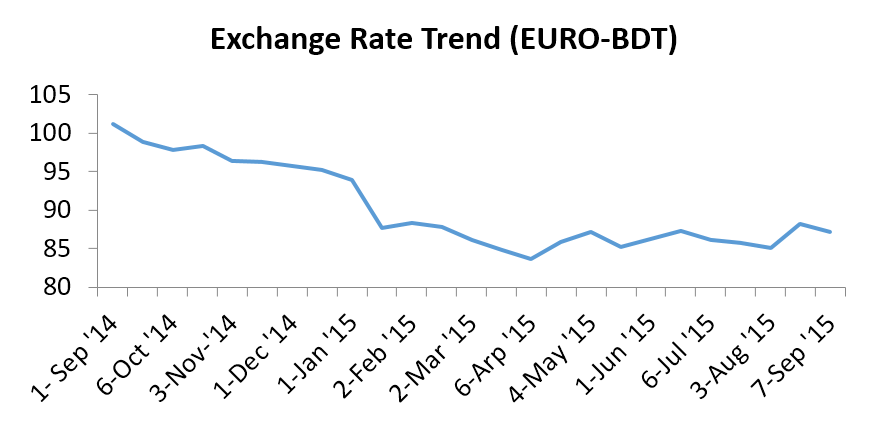

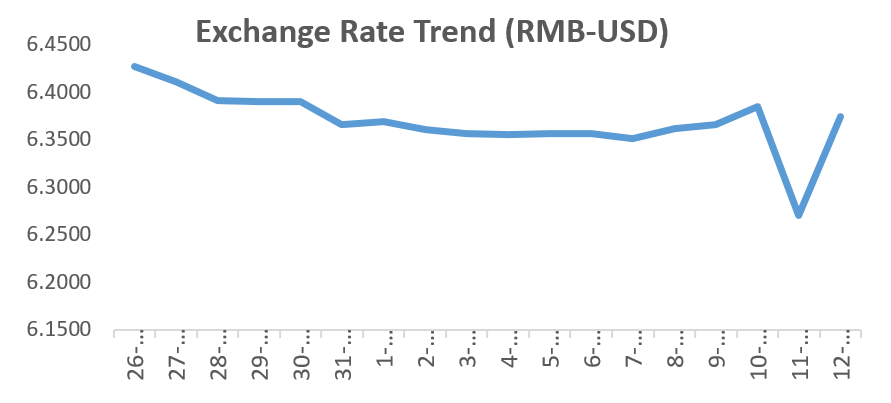

Depreciation of the Euro against all major currencies has been due to the Eurozone crisis spearheaded by Greece’s debt default. Over the last year, Euro has depreciated by almost 18% against BDT which is bad news for the local apparel sector. EU countries collectively import 61% of Bangladesh’s apparel export and the depreciating euro means Bangladeshi apparel has become more expensive to import. As the Eurozone crises persist, Euro is not expected to gain value soon which may hurt future export to Eurozone. The recent devaluation of the Chinese RMB also means Chinese products will artificially get more competitive in the international market. However, raw materials procured from China will become cheaper contributing to the cost competitiveness of Bangladeshi apparel.

The USA, the single largest importer of apparel from Bangladesh, has recently canceled GSP for Bangladesh’s export citing a number of reasons. Although apparel was never part of GSP, BGMEA had been lobbying hard to get tariff-free access to apparel. The recent development will be a major dent in ensuring free access to Bangladeshi apparel.

Turkey, considered to be an emerging export destination, has recently imposed a tariff on Bangladeshi apparel. As a result, Bangladesh’s apparel export to Turkey has plummeted to USD488 M in FY14-15 from USD623 M in FY13-14.

The Game Plan

Ending Note

Mckinsey, in their 2012 report, had projected that Bangladesh’s apparel sector export will grow to USD 42 Billion in 2021. Local industry leaders have earmarked a USD 50 Billion RMG export target within 2021. All these promises will turn hollow if concrete steps are not undertaken for ensuring sustainable growth for the sector.

Time is running out!

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights