GET IN TOUCH

- Please wait...

Background

As time passes, the world experiences development in all sectors. Development leads to urbanization, reflecting economic growth, which brings upon infrastructure development and construction. Cement is a major component in this chain. Hence, when dreaming about a futuristic world with tall skyscrapers, massive bridges and other concrete structures, we need to keep in mind that unless and until there is a great discovery of a substitute, without cement it will be impossible to see that future in reality.

There are mainly 27 types of cement, which can be grouped into 5 general categories and 3 strength classes: ordinary, high and very high. Cement mainly used for construction can be segregated broadly into two categories, hydraulic and non-hydraulic, differentiated by the ability of cement to solidify in presence of water.

Global Perspective

In a recent research conducted by International Cement review, global demand for cement had doubled within the decade between 2002 and 2012, from 1.8 billion MT to 3.7 billion MT. This was reflected in the high CAGR between 2002 and 2015 (7.4%), than the previous decades (4.3%).

However, the estimated CAGR between the year 2012 and 2017 dropped to 4.3%, which was 6.2% between 2007 and 2012. This is in reflection to global economic trends and the consequent effects on heavy industries throughout the globe.

Moreover, the 2008 financial crisis had severe impact on the world economy. In many areas, the housing market also suffered, resulting in evictions, foreclosure and prolonged unemployment. This greatly depressed the real estate sector. Since then, the global cement industry has undergone major changes, like industry wide consolidation and increased operational efficiencies.

The newly completed merger of Lafarge and Holcim to form Lafarge-Holcim was the second biggest merger of 2015, forming a company worth USD 50 billion. The deal is expected to become the most advanced group in the building material industry and save the companies USD 1.9 billion annually (New York Times, 2014). Merger of this scale would obviously raise regulatory concerns as the industry is already highly competitive, with regular races to the bottom in terms of price.

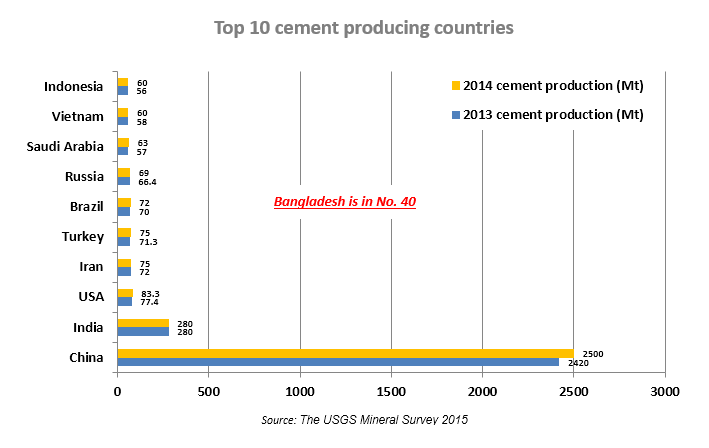

However, in spite of the financial crisis, the global cement production has continued to grow. According to the United States Geological Survey, in 2014 global cement production grew to approximately 4.18 Bn Tonnes, up from 4.08 Bn Tonnes in 2013. Among the global producers, China and India are by far the largest in the world. Further, capacity expansions in China, India, Saudi Arabia, UAE, Turkey, Egypt, and Brazil are underway and at a significant pace and is expected to pick up in the coming years. Lafarge-Holcim was the second biggest merger of 2015, formed mainly to gain market power and increase efficiency.

Bangladesh Scenario

The birth of the cement industry in Bangladesh dates back to 1994. The local demand was huge as the consumers substituted imported cement with local products. Later, in 2003 M.I Cement first started exporting (Crown Cement). Till now, several cement producers have exported their products to the seven sister zone & West Bengal of India, with a good potential to further accelerate the export volume.

Since, 1994, more than 120 companies have registered as cement manufacturer, of which 75 actually came into operation and the rest (smaller companies) were forced to shut down. The reason was mainly financial inability to compete with the national players, geographical disadvantage and utility supple shortage.

Demand Factor

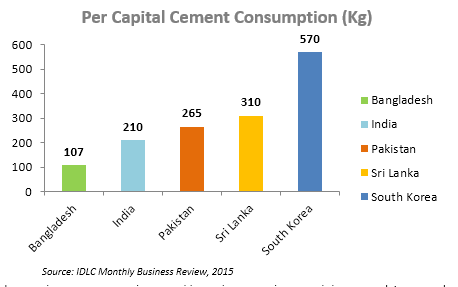

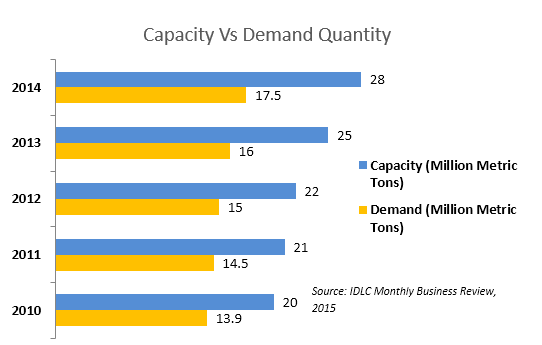

Currently, the cement industry of Bangladesh is the 40th largest market in the world. Bangladesh is one of the fastest developing countries and is thus expected to have major infrastructure, housing and services development in the coming years. Thus, expecting a growth in demand for cement is considered logical. Since the liberation war in 1971, major urbanization and industrialization took place in the country, which led to a rise in demand for cement. As the companies saw an opportunity in the field, they undertook capacity expansion plans. However, multiple factors like, delay in the construction project of Padma Bridge, political unrest, economic slowdown and also the downfall in the real estate sector have greatly impacted the industry growth. Thus, the expectations regarding the increase in demand were not met.

For commodities like cement, which requires strong consumer confidence, competitive price is not the sole factor ensuring the demand,![]() is also important. Thus, global players have an advantage in this regard, as customers finds them more trust worthy due to their worldwide presence. On the other hand, senior local brands are also being able to sell their brand name as they have gained customer loyalty. Hence, the new comers are likely to face a difficult time entering the market, unless they plan for higher marketing budget.

is also important. Thus, global players have an advantage in this regard, as customers finds them more trust worthy due to their worldwide presence. On the other hand, senior local brands are also being able to sell their brand name as they have gained customer loyalty. Hence, the new comers are likely to face a difficult time entering the market, unless they plan for higher marketing budget.

Apart from this, the sector experiences a seasonal demand cycle, where demand reaches its peak during the dry season (September/October to April/May), and falls during monsoon (May/June to August/September). During the peak season the companies carry out multiple promotional activities, which includes giving incentives to the agents and employed executives if targets are met.

Supply Factor

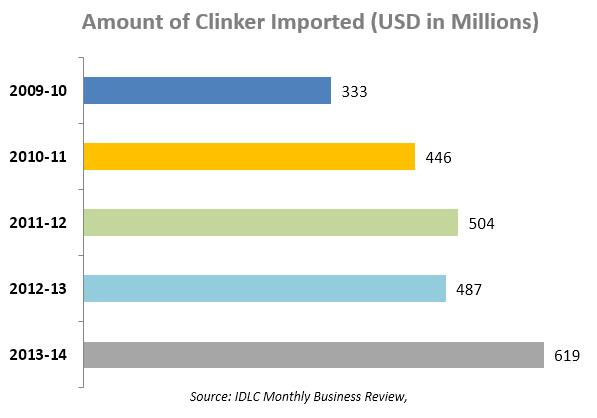

Though the cement industry is highly competitive, the bargaining power of the customers is unable to bring prices down as the producers struggle hard to achieve economies of scale. Production is heavily dependent on imported raw materials such as clinker, 80% of which is currently imported. Bangladesh lacks the mineral resources such as limestone and is unable to meet the demand of clinker by itself. However, among 30 cement producers only two have the facility to produce clinker. One of them is Chhatak cement Factory and the other one is Lafarge Surma Cement Ltd. Lafarge itself meets 10% of the clinker demand of Bangladesh.

Another major factor is power as production of cement requires huge supply of electricity. The majority of this supply is met by the national power grid. However, large companies are trying to use captive power plants to reduce the cost and ensure stable power supply.

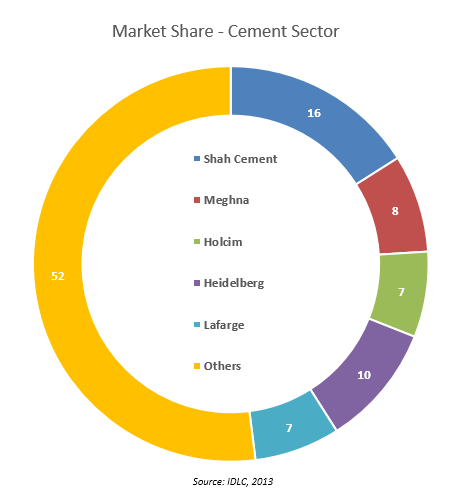

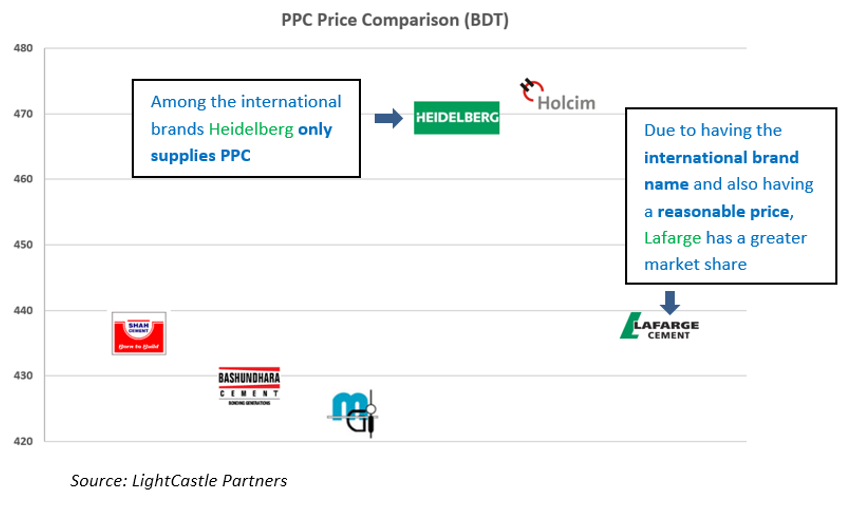

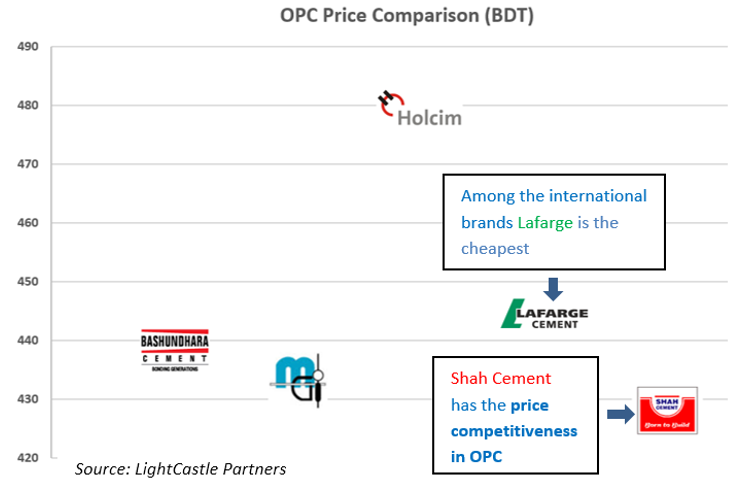

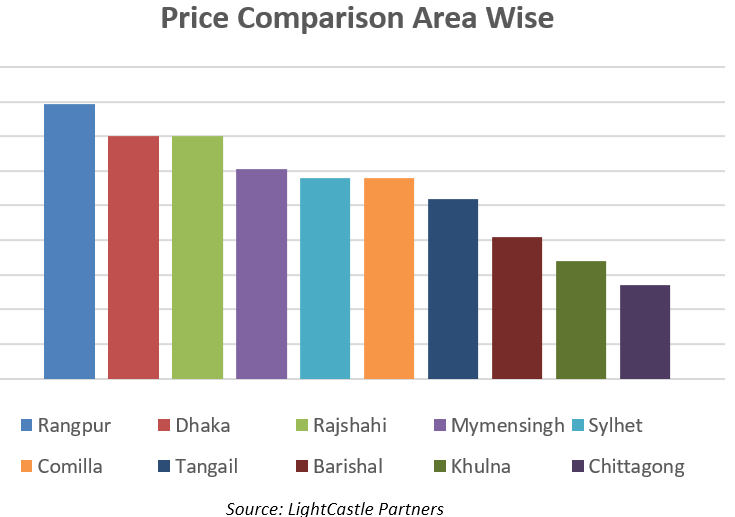

Price Comparisons

Cement prices vary a lot in different locations, mainly due to the transportation cost associated. Holcim’s and Heidelberg’s products are the most expensive on average. However, Heidelberg only supplies PPC. On the other-hand Meghna sells at a much cheaper rate compared to the others. Prices are lower in the central regions like Dhaka, Tangail and Mymensingh. Areas close to the factory are able to provide relatively cheaper products, such as Chittagong and Sylhet.

As the number of bags purchased increased, prices tended to go down. In 80% of the regions, prices went down from 50 bags onwards, by BDT 5 to BDT 10. When number of bags purchased exceeded 200, some prices across retailers decreased by about BDT 5. However, at this volume, the retailers would source directly from the dealers and bear the carrying cost, giving the customers an effective discount.

Future projections

Though, the sector has experienced a falling growth rate over the past few years, it’s worth noting that the growth rate was still positive. Market insiders expect the industry to grow by 20 to 25 percent over the next few years (Cement Association 2015). Initiatives like undertaking the construction of the Padma Bridge and government’s plan to use RCC pavements in highways may boost the demand in future.

However, newly formed giants like LafargeHolcim, and Heidelberg Cement’s recent acquisition of Italcementi, might seriously disrupt the market affecting the already competing market players, who are still surviving by charging marginal costs. On the other hand, presence of strong global players, including strong local brands are making it even harder for the smaller companies to survive

Further, the export market has little potential because Bangladesh doesn’t have a domestic source for raw materials (clinker), resulting in higher costs. Secondly, transportation cost is a major factor, since transporting voluminous products are expensive. For ensuring competitiveness, Bangladesh will have to focus on export to nearby regions, such as the seven sister states in India.

Mahir Abrar Nikhat is a research associate at LightCastle Partners. He graduated from the University of Hong Kong, majoring in Economics and Finance and is currently doing his masters at North South University, in Economics.

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights