GET IN TOUCH

- Please wait...

Since 2011, mobile financial services (MFS) have proved to be the finest integration of finance and technology in Bangladesh, where only 29.1% of the adult population had access to financial services, whereas 78% of the total population possessed mobile phones. MFS has significantly contributed to rural-urban fund flow as efforts are being made to popularize mobile money as a viable alternative to physical and plastic money. Further growth of MFS would ensure higher penetration at the Bottom of the Pyramid (BOP) market and contribute to the growth of online e-commerce transactions.

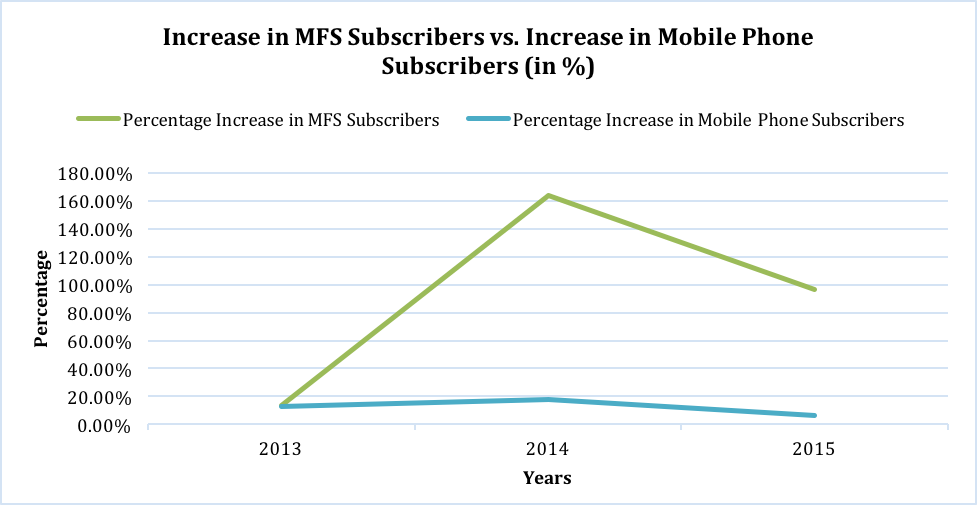

The following figures resemble how fast MFS is growing.

Till date, there have been 10 MFS providers in Bangladesh, among which Brac bank’s brash and Dutch-Bangla Bank’s mobile banking services are the top players. According to the latest report by USAID, as of February 2015, transactions worth USD 1.4 billion were made through MFS, which was USD 400,000 during the same period in 2014.

As per the survey conducted by USAID, about 99% of mobile phone owners reported having a bank account. About 86% of them used their accounts for savings purposes. This implies a strong inclination of users toward saving accounts, which could be capitalized by increasing interest rates for fostering the growth of the MFS sector. Bill payment is another popular utility for MFS users.

As of February 2015, a total of 543,000 agents have been serving 25.87 million subscribers. About 71% of all mobile financial users have an agent within one kilometer of their reach, whereas only 41% of the bank account holders have access to bank branches within a similar distance. About 91% of the MFS users and 88% of non-MFS users ranked lower transaction costs as the most important priority to them, and 61% of the MFS users stated that they could save money because of lower fees. On the other hand, 90% of the users stated that MFS accounts had been easy to use in terms of checking balances and conducting various transactions, which clearly shows that the industry has done a great job in terms of eliminating procedural complications.

Over the last few years, the e-commerce industry has been experiencing significant growth. In 2012, Bangladesh Bank had launched National Payment Switch to nurture electronic payment and perk up the e-commerce industry. However, due to cost concerns, the steps didn’t positively impact the majority of the population in the digital space. On the other hand, since 68% of MFS transactions, according to the USAID report, originate from urban and semi-urban regions, the simplicity of the transaction process of the service has greatly contributed to user penetration. Almost all portals currently accept mobile money as a preferred payment method. As of 2014, online shopping transactions accounted for BDT 200 crore, growing at 30% every month (The Daily Star, 2014).

While more than 60% of the population originates from the rural areas of the country, in terms of financial services, only microfinance institutions (MFI), including Grameen Bank, Brac Bank, etc., have been able to facilitate this particular segment of the population financially. Due to the low literacy rates, these people have long detached themselves from financial inclusion due to the fear of maintenance costs and procedural complications. In 2012, the government ruled to open at least one out of five branches in rural areas. Though this resulted in a 57% increase in the physical presence of banks in rural areas, the share of these branches stayed static at 17% and 12% in terms of total deposits and advances. Mobile financial services have become popular for sending and receiving money among account holders. The rise of MFS has contributed to eliminating over-the-counter (OTC) transactions. Conceivably, better integration between MFI and MFS would serve the population better. Implementing the native language within the USSD platform to aid the minimal literacy would also add value and make it more comprehensible to the people leading to higher adoption.

Finally, it can be undoubtedly stated that MFS has the potential to further boost the country’s economy by facilitating fund flow across the economy, prepping up online transactions, and providing financial inclusion for the BOP population. Further expansion of MFS will be a game-changer for the country’s growth story.

The analysis was conducted by Md Sifat Bin Raquib, a Junior Associate at LightCastle Partners. He can be reached at [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights