GET IN TOUCH

- Please wait...

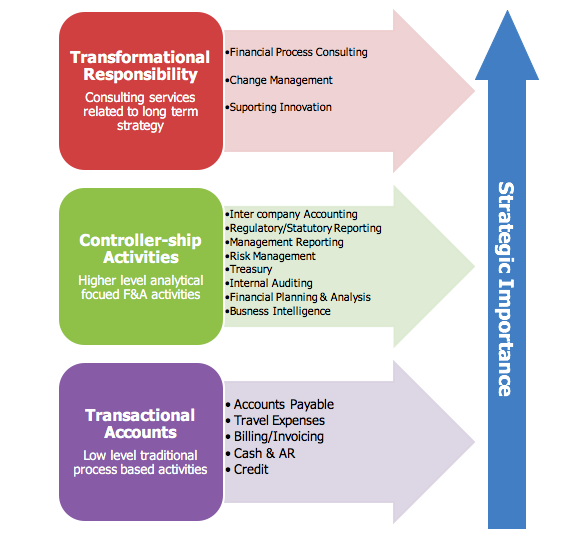

Finance and accounting outsourcing (FAO) was originally a service offering a value proposition driven by cost savings and efficiency. However, as the market matures FAO solutions tend to be more strategy focused as depicted below:

The above value chain refers to the series of departments which carry out value creating activities to design, produce, market, deliver and support a company’s product or service.

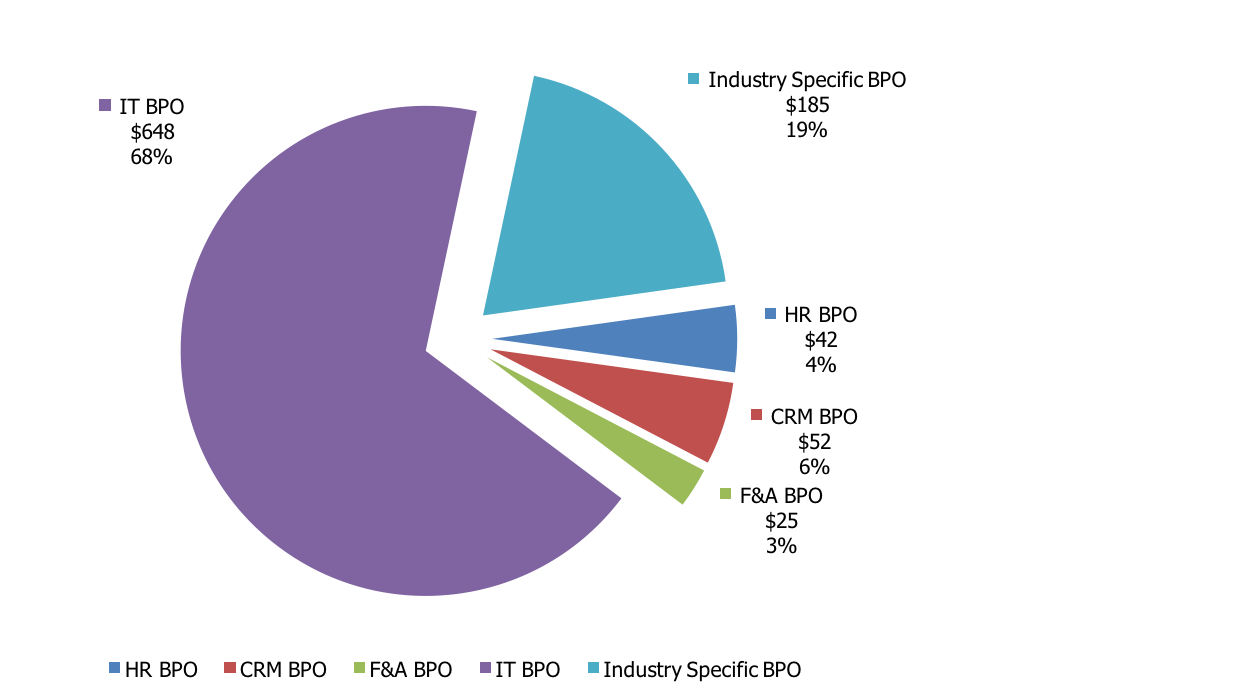

The global BPO & IT services market was worth approximately $952 billion in 2014 out of which IT Services was 68% at $648 billion and BPO was 32% at $304 billion. An approximate break-up is shown below:

The overall BPO & IT Services market is set to grow approximately 5.7% in 2015 taking it to $ 1 trillion. FAO is expected to grow to at least 4.5% of the total pie in 2015 due to enhanced interest in this sector as discussed in detail below.

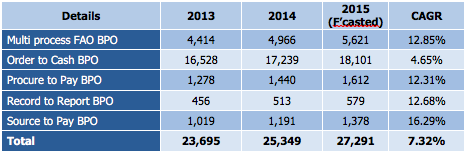

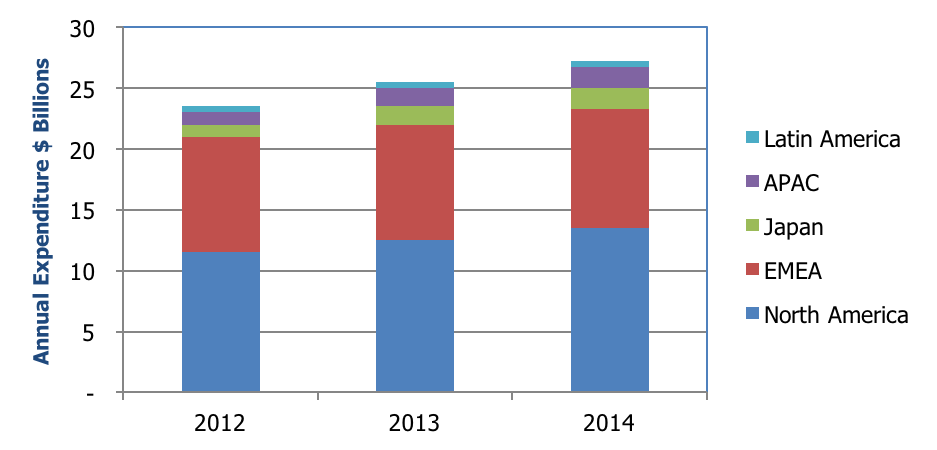

$25 billion was spent on FAO in 2014up from $23 billion in 2013 which is expected to cross $27 billion in 2015 growing at a CAGR of 7.32% which can be approximately broken up in the following way including comparative figures in $ millions:

As per publicly available information and forecasts, the FAO market is expected to grow at a CAGR of 8% annually through 2017. Research into FAO shows that most companies still prefer to manage F&A functions in-house but the attitude has slowly shifted towards outsourcing as senior management push for further cost efficiencies and process standardization. Over 90% of BPO engagements meet these criteria and 2015 will see a number of the new medium to large enterprises seeking FAO initiatives. However, the FAO market is still in a nascent stage and there is a long way to reach maturity as shown in Figure 2 where FAO is only 3% of the total IT & BPO industry globally. The industry is also experiencing a move towards multi-process (at least two F&A processes) FAO in 2015 as companies are moving away from the traditional single product outsourcing.

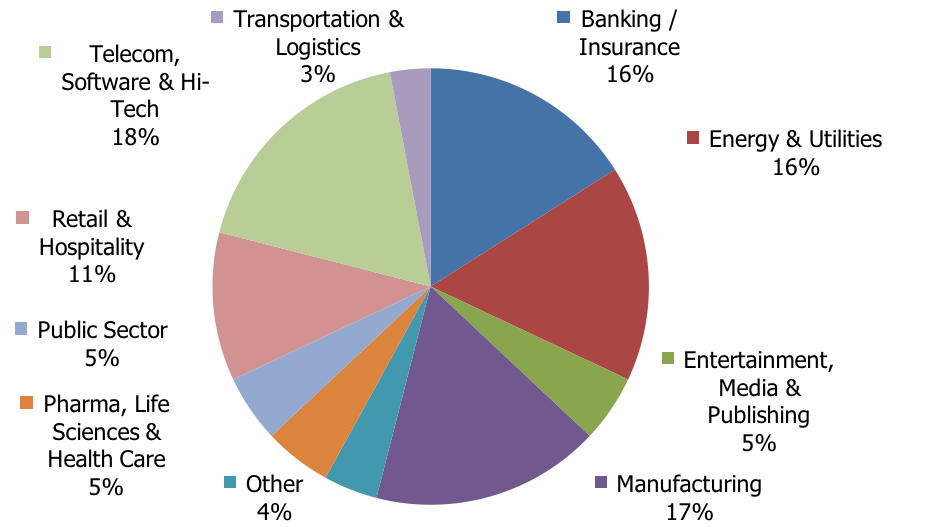

The key growth industries from 2015 onwards are expected to be telecom, software, IT, high tech, media, retail, and hospitality. Banking, financial institutions, and manufacturing still dominate a large portion of the FAO market but growth has slowed in recent years as shown below.

However, forecasts by experts expect the CAGR of Media & Publishing, Public Sector, and Telecom, Software & Hi-Tech to be in double digits from 2014 to 2017. Growth in the dominant Manufacturing and BFSI is expected to hover around the 5% mark. Growing public sector reforms in developed economies are seeing a move toward efficiencies and cost savings shifting their focus toward BPO. Ease of regulations in other countries also means government agencies will be allowed to outsource the certain process to the private sector. Technology and hi-tech industry being the most innovative and forward-looking outsource most of their processes in order to focus on core competencies. Another sector to look out for in the very long term is new entrepreneurs (mostly in the “Others” category in Figure 5) who initially set up looking to achieve maximum efficiency and cost savings in F&A processes thereby outsourcing completely. Subsequently, if successful expansion takes place they prefer to continue with this model. In the next decade, various schools of thought predicts that in-house F&A may almost disappear in small to medium non-listed enterprises.

North America still retains the highest market share of the amount spent on FAO globally at close to 50% followed closely by the EMEA region at 40%. However, Japan and APAC have been spending more and more on FAO in recent years due to changes in culture and the recent increase in salary and associated costs in the last decade, and is expected to grow significantly from 2015 through 2017. Latin America remains small in terms of the FAO market due to the availability of cheap labor and lower costs compared to other regions. This is not expected to change in the next 5-7 year horizon.

To be continued…

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights

![Mitigating Risks for Matarbari DSP: Drawing Insights from Hambantota Port [Part 2]](https://www.lightcastlebd.com/wp-content/uploads/2024/07/IMG_0612-1024x682-1.jpg)

![Matarbari Deep Sea Port: Unlocking the Economic Potential of Bangladesh [Part 1]](https://www.lightcastlebd.com/wp-content/uploads/2024/07/matarbari.png)