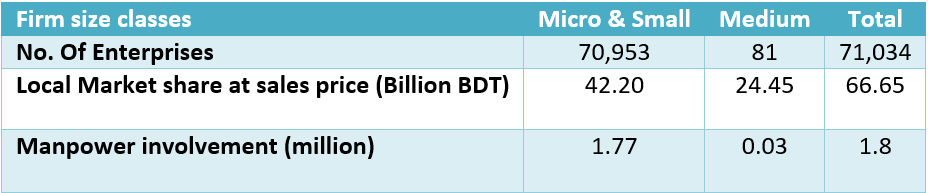

The furniture industry in Bangladesh has been experiencing healthy growth over the last 6 years. The domestic market is exhibiting an upward trend and is currently worth BDT 67 Billion. (Source: EU Technical Report, 2012) Also, within that time, exports of wooden furniture have increased by CAGR 104% to USD 38.94 Million (source: EPB), while the total number of enterprises has grown by 68% to 71,034 (source: EU report).

Figure: Bangladesh Furniture Export Trend (EPB)

Factors Contributing to Growth

Some major factors contributing to the sustained growth of the furniture industry is provided below:

- Growing Domestic Demand: According to the latest BCG report on the growing consumer class, the Middle and Affluent Class (MAC) population currently stands at 11.7 M and, is expected to triple within 2025. This emerging class has growing disposable incomes which are being spent on consumer durables, including furniture.

- Access to Credit: Currently, Bangladesh has 60+ banks vying to capture the retail banking segment. Many of these banks offer credit cards and consumer loans which are easily accessible to the MAC segment. Preferential credit card terms make purchase decisions simpler for users planning to buy furniture.

- Improving Supply-side Capabilities: Part of this growth can be attributed to a stylistic shift in furniture design. The country’s carpenters have recently begun incorporating styles from their foreign counterparts, increasing the range of options available for consumers, looking for one-of-a-kind aesthetics. This is resulted in consumers regularly changing their furniture.

- Inexpensive Labor: The shift can also be attributed to the presence of inexpensive labor in the industry, an industry that is labor-intensive. Laborers in most countries where furniture is produced are paid more than $120 a month, while Bangladeshi laborers are paid between $37-120 a month (EU Technical Report).

- Backward Linkage: According to the EU study, 40% of the raw materials used by the industry come from domestic sources. Forests in Chittagong Hills and the Sundarbans are the largest provider of quality timber in the country, with forests covering areas over 10,600 Sq Km.

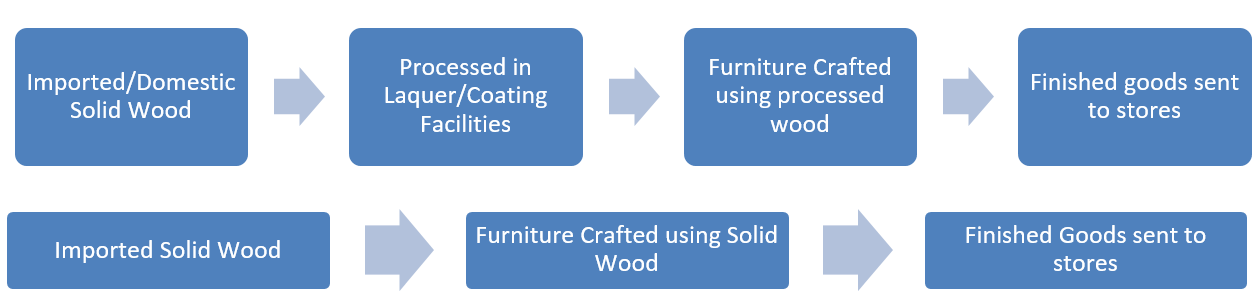

Value Chain Analysis

There are mainly two classes of wood used by furniture manufacturers. One is Solid wood and the other is Processed Wood. The Solid wood needs to be seasoned in the order for it to be sturdy and aesthetically appealing, however, there are very few seasoning plants in Bangladesh and those that do exist are owned by specific furniture manufacturers. The processed wood on the other hand needs a good laquer/coating facility, which only the mid-high tier furniture manufacturers have.

The chief raw materials used are wood, laminated board, wrought iron furniture, processed wood & medium density fiber wood, particleboard, and rattan bamboo. However, most of these materials need to be imported. Of the woods; Tic, Gamar, and Hardwood come from Africa, while Barmatic wood comes from Myanmar. The tariffs on these materials are prohibitively high. The import duties for all solid wood are at 10.72% while the duty on particle wood is 92.3%. This pushes the price upwards making it harder for producers to provide affordable furniture

Manufacturers are unwilling to import processed wood because of the high import duty of 92.3%. The timber used in the industry is available from local forestry and import sources however, due to an increase in reforestation and government-enforced protective forest zones; the availability of timber is sharply declining.

A Growing Demand

The domestic furniture market is worth more than BDT 67 Billion (EU Technical Report). According to the latest BCG report, wealth is no longer centralized in Dhaka and Chittagong. Thirty-six cities already have more than 100,000 in the Middle and Affluent Consumer (MAC) class, with the number of cities expected to rise to 63 in the next 10 years. These MACs have enough income to afford luxury products and have biases towards branded ones. Hence, an increase in the number of MACs will lead to an increase in the demand for branded furniture.

There is also a preference towards ‘trading up’ among consumers in Bangladesh, particularly in the case of durable goods (like furniture). As income levels rise people substitute their durables with ones that are more convenient and provide greater comfort.

Finally, some nascent demand exists in the shipbuilding industry. Bangladesh is expected to capture 2% of the ship-building market within the next 4 years. This will provide demand for furniture in the newly constructed ships.

The Competition

The industry is very competitive. Due to the sheer number of SMEs, the price of furniture is highly competitive in the middle and lower segments of the market. The larger firms have captured a small segment mostly catering to MAC consumers who don’t mind paying a premium for quality and brand.

Source: EU Technical Report (2013)

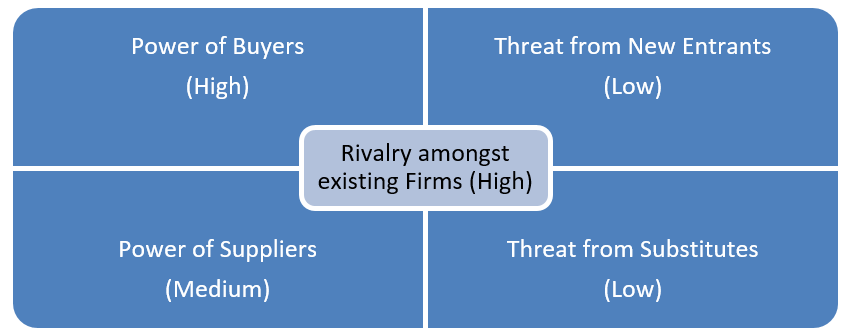

We have further analyzed the market using Porter’s five forces framework.

- Bargaining power of buyers: The Industry has over 70,000 enterprises, which exhibits traits of monopolistic competition. In a monopolistic competition firms take the prices of their competitors, with limited pricing power; hence the bargaining power of the buyer is very high. However, the top 6-7 firms catering to the top segment of the market tend to have higher bargaining power over buyers.

- Bargaining Power of Suppliers: Due to the recent reforestation efforts the supply of raw materials from the domestic market has decreased. This leaves furniture manufacturers with fewer choices when it comes to choosing a suitable supply source. However, the choices abroad are still abundant. Countries like Myanmar, India, and African countries are reliable import sources.

- Threat from substitutes: There are no direct substitutes for furniture as a whole. Although furnitures are available made from steel or plastic furniture, they are not popular enough to pose any major threat to the market for wood-based furniture.

- Threat from New Entrants: The market is already crowded and probably will grow even more due to the lack of entry barriers. However, these new entrants will not pose a threat to the market share of existing enterprises due to intense competition and razor-thin margins. The top segment could possibly be disrupted by the entrance of a big brand e.g. Ikea since Bangladeshi consumers are more biased towards brand image (BCG report)

- Overall Rivalry: We can see now that the rivalry among the existing enterprises is fierce, due to the sheer number of enterprises that exist in the market and the threat that exists from the possible entrance of big foreign brands.

Top Names

As stated previously, there are more than 70,000 enterprises that produce furniture in Bangladesh however the market is dominated by a few large companies; some of them are as follows.

- Otobi: Starting off in 1975, Otobi is one of the pioneers of Bangladesh’s furniture industry. They have the largest distribution network with over 18 retail and 288 exclusive dealer outlets. In total, it has over 450 selling hubs across the country.

- Akhtar: The company started off as Akhtar Furnishers in 1976. They have seven industrial units spanning over 75 Acres of Land and sell a range of products including foam, furniture, door, timber coatings, mattress, and adhesive. They have eight large showrooms in Dhaka and a few more in another city. It has also established the Akhtar Furniture academy, the first and only private institution in Bangladesh that specializes in teaching furniture production.

- Navana: Navana Furniture Limited was established in 2002. It currently has over 80 outlets across Bangladesh. They import all of their major raw materials and their production plant is fully integrated. They mold, design, assemble and test the materials by themselves.

- Hatil: Established in 1969, Hatil started off as a timber company. It rebranded itself as a furniture producer in 1989. They currently export to countries including (but not limited to) the USA, Canada, and Australia. They are also the only FSC certified furniture manufacturer in Bangladesh.

Closing Remarks

The furniture industry is under the bondage of import duties. Experts suggest that easing the extent of the duties can double sales in the industry. However, even with the restrictions, the industry is expected to grow. Fueled by increasing demand from millennials entering the job market, a steady GDP growth rate of 7%, and an abundant supply of inexpensive labor, the furniture industry is on course to become a large contributor to the country’s exports.

Research has been conducted by Ishtiaqur Rahman, Junior Associate at LightCastle Partners. Check out the LCP drive for downloading sector-specific reports: www.lightcastledata.com/drive

WRITTEN BY: LightCastle Analytics Wing

At LightCastle, we take a systemic and data-driven approach to create opportunities for growth and impact. We are an international management consulting firm which creates systemic and data-driven opportunities for growth and impact in emerging markets. By collaborating with development partners and leveraging the power of the private sector, we strive to boost economies, inspire businesses, and change lives at scale.

For further clarifications, contact here:

[email protected]