GET IN TOUCH

- Please wait...

Bangladesh is one of the few countries in the world which provides piped gas connections to households for cooking purposes. Although LPG (Liquified Petroleum Gas) containers have been available for sale since 1980s, supplied by state-owned BPC (Bangladesh Petroleum Company), it failed to grab market share until the enactment of government’s policy restricting fresh connections in households.

What is LPG?

In Chemical terms, LPG consists of a predetermined mix of Propane & Butane and contains higher calorific value than natural gas. Autogas, a popular form of LPG is used as a ‘green’ automotive fuel around the world. Not only it is good for engine and environment (free of lead, very low in sulphur & other metals), it can potentially save costs compared to other fossil fuels.

1) Macro-economics of LPG industry demand-supply

Demand side

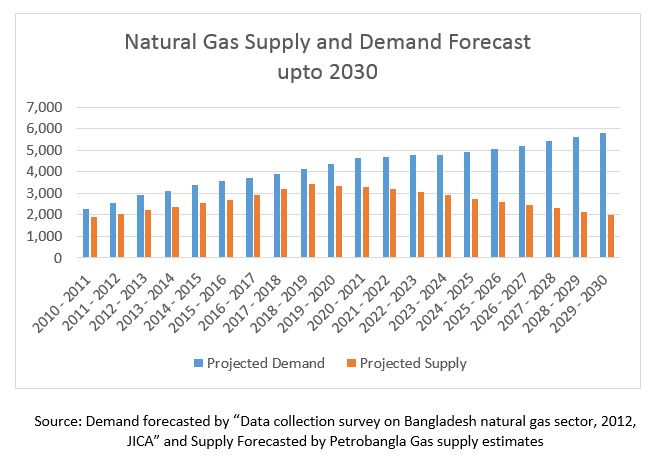

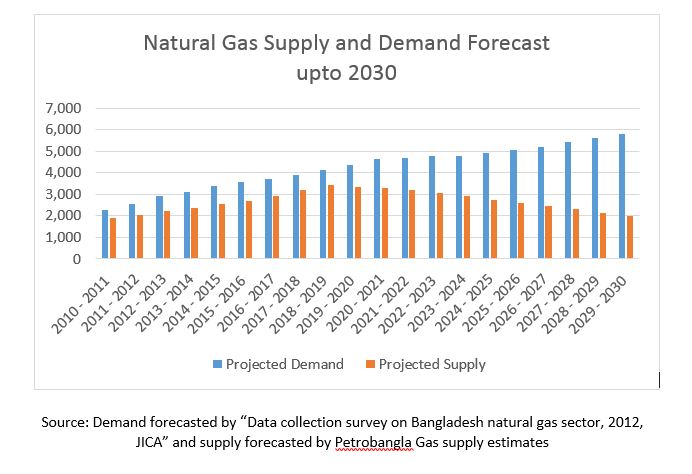

The rising demand for LPG and other energy sources is a consequence of depleting gas reserves of the country. As of 2015, the natural gas reserves of Bangladesh is 14.16 trillion cubic feet and is enough to last till 2031, if current rate of extraction is maintained, according to Government statistics. The rapid use of natural gas in power production has been the main source of gas consumption, since it contributed to 56% of domestic energy demand, depleting gas fields and putting pressure on energy sector. Titas gas is already rationing gas connection to higher priority areas as of 2016. The current gas production from the 20 operating gas fields within the country yield about 2,500 mmcdf (million cubic feet per day), and is speculated to reach peak production of 2,700 mmscfd within 2017, and then decline. In FY 2015-16, overall gas demand in the country has been estimated to be 3,200 mmscfd (petrobangla data), which means a 30% deficit on total demand. An annual shortage of 500 mmscfd natural gas shows the need for diversifying the energy requirements. The deficiency of Natural Gas (NG) will only increase and it will have an overall impact on electricity generation, fertilizer, transportation and domestic sector.

LPG is mainly used by households for cooking and by some light engineering workshops, as fuel for wielding. Increase in LPG demand has been contributed by unavailability of fresh NG connections households, increasing price of kerosene and decreasing accessibility of firewood. Bangladesh’s LPG demand is only 2% of total oil demand, and less than 0.01% out of the total energy demand. However, LPG demand is expected to grow significantly as an alternative to households’ cooking fuel and transportation fuel (in the form of Autogas).

Gas demand forecasts for Bangladesh is expected to grow with increasing number of industries and households in future. While LNG import is expected to compensate for the industry gas demands, LPG is expected to be an alternative for household gas use.

Currently, the residential sector occupies about 13% of total natural gas consumption. In terms of number of consumers, about 2.8 million household consumers are now using 330 mmcfd gas (13.06%) of total gas production according to the national Energy Division. Even with a power conservation policy, the projected demand for gas in 2030 will be at least three times of demand.

Supply Side

Availability and improving the supply system are two major constraints for the supply side. The current demand for LPG in 2015 was 150,000 Tonnes and currently more than 80% of the LPG demand is met by import and the state-owned BPC supplies the rest 15-20%. The source for government supply are from government oil refineries, since LPG can be produced as a by-product of oil extraction.

Private sector imports are from Singapore, Malaysia, Saudi Arabia, Abu Dubai and Kuwait. The standard import price is the Saudi Aramco (the state-owned oil company of of Saudi Arabia) monthly contract price. When buyers order bulk LPG from international market, they have to pay that month’s Aramco Contract Price and add the freight per ton charge (for shipment to Bangladesh). While the government subsidizes their portion of LPG, the importers sell their products in line with import price.

2) Local LPG Market Status Quo

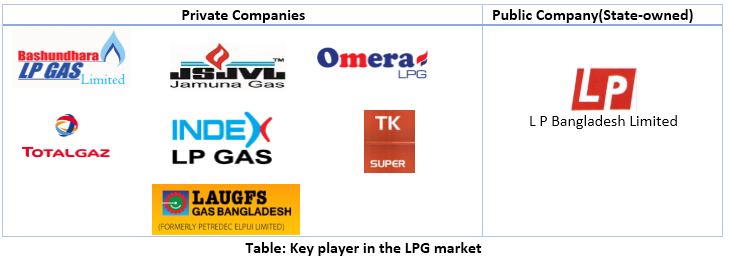

The key players currently working in the LPG industry are:

Basundhara, Jamuna, Omera, TK Gas are local companies whereas TotalGaz and Laugfs Gas( corporate brand name Kleanheat gas) are foreign companies. Bashundhara, TotalGaz, Jamuna and Cleanheat each have production capacity of one lakh tonnes. Only Bashundhara and Jamuna make their own LPG cylinders, while the others import them. TK Gas (Supergas) and Bin Habib Bangladesh Ltd do not import LPG. They buy gas from importing companies and bottle them from their own plants.

The Government has granted more than thirty new licenses to private operators, who are willing to set up downstream LPG operations with five new players coming up with Tk 900cr in investment.

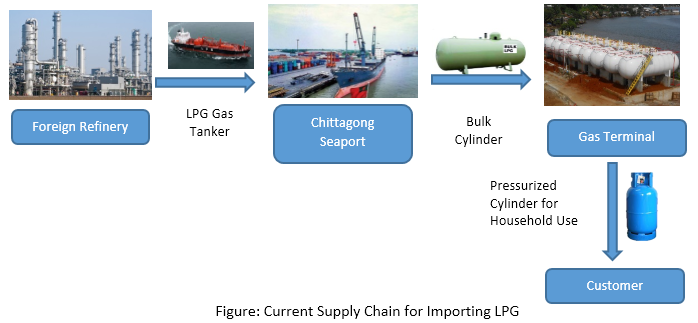

The current operations of the companies can be broken down as: Buying bulk LPG from foreign refineries or traders – Shipping the bulk LPG to their terminals in Bangladesh via seagoing gas carriers – Storing the bulk LPG into spheres or bullets via jetty pipeline – Finally filling the gases into pressurized cylinders for onward distribution to the final consumers. Ideally, once the customers use up all the gas, the empty cylinders are sent back to their respective operators for refilling.

Since the contract price is transparent and remains static for a month, the buyers who pay the most competitive freight charges becomes advantageous. The freight charges are reduced with the increasing size of the Bulk LPG Cargo. For example, the freight per ton cost of a LPG carrier of 5000 MT capacity is much lower than the freight per ton cost of a 1500 MT LPG gas carrier (Based on similar length of travel).

Since the discharge terminals for the current LPG import companies are beside rivers with severe draft restrictions (e.g. Chittagong and Mongla), their jetties can receive gas carriers of maximum of 2,500 MT capacity. So LPG operators have to pay higher freight per ton charge for Bulk LPG cargo, compared to international operators. However, if the new LPG licensees set up their plants near high draft water bodies e.g. South of Chittagong City or near Moheskhali, their jetties will be able to discharge large gas carriers up to 5,000 MT Capacity reducing the price of the end-product LPG cylinders.

The existing price of LPG is mostly market driven. Plant-gate prices of 12kg LPG cylinder of Kleenheat or Petragaz is BDT 1,200, Bashundhara Gas BDT 1,220, Total Gaz BDT 1,180, Jamuna Gas BDT 1,130 and Omera LPG BDT 1,050.

3) Growth Potential of LPG industry for the future

The current LPG imports require 5% customs duty, 15% VAT, 5% advance income tax and 4% advance VAT. To encourage LPG use, GoB proposed the Duty, VAT rationalization on imported LPG in the FY2016-17.

The current price of LPG is two to three times higher than that of the pipelined gas and may not be affordable for the average households. While a rural family would spend 4-7 % of their monthly income on traditional solid biomass as fuel for cooking, LPG at the current market price would be 25%. Subsidy to LPG may work up to some extent to increase affordability but, some policy modifications are needed to make LPG affordable to the average households.

The positive side for the LPG pricing is, more local and foreign investors are showing interest for investing in the LPG sector, since demand outstrips supply. If the existing pipe gas network can be used for distribution of PLG, it would cut the total cost drastically.

An LPG plant is to be installed on a 10 acre land in Chittagong, with import and storage facilities. The plant will have a capacity of 100,000 million tonnes and a cylinder manufacturing unit. Another LPG cylinder and accessories plant will be setup in Tangail.

The budget of FY2016-17 has rationalized the Customs and Supplementary duty which may bring in positive impacts on LPG cylinder price for end users. The LPG autogas cylinder could be a lucrative choice for public and private transports in the face of rising CNG demand. The current trend of using CNG for transport vehicles can be replaced by the environment friendly LPG.

With positive government reinforcements through favourable policies, new players are expected to enter market, accelerating penetration within the urban, peri-urban and rural areas. Alongside, growing urbanization led by rising income and living standards, will increase potential demand for LPG among households.

Author

Imran Chowdhury is a business consultant at LightCastle Partners. His passion for research can only be matched by his love for photography. He can be contacted at [email protected].

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights

{kind=link}