GET IN TOUCH

- Please wait...

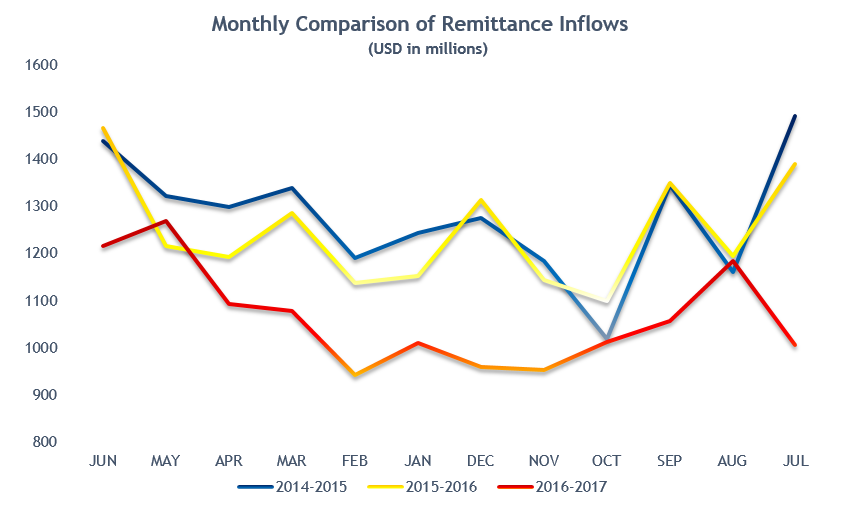

Global remittance flow has declined for two consecutive years- for the first time since the turn of the millennium. The last time there was a decline- it was during the global financial crisis. The World Bank expects world remittance to rise to a record high of 600 billion dollars in 2018, suggesting that the current downturn is just a blip. But what actually caused it?

Economists and market analysts provide explanations from different viewpoints to why the slump is happening.

EXCHANGE RATE: Bankers say that a major reason is the adverse exchange rates, that it discourages workers sending money through official or legal networks. These transactions do not appear on records.

STRICTER MIGRATION POLICIES: Policy makers and government officials from Asian and African countries blame stricter migration laws of US and EU member countries. Remittances from USA fell at a crashing rate. With the Trump administration’s strict migration laws, even residents with green cards fear that if they leave the country- they might not be allowed back in. Rational or not, these fears drive them to save more and send less.

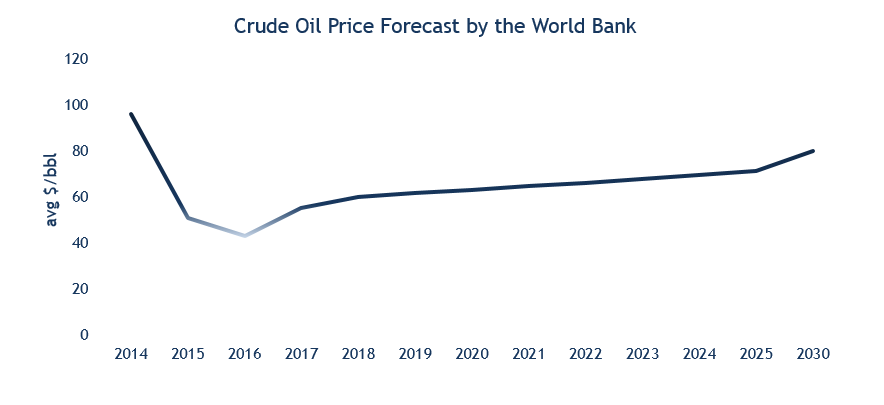

Nevertheless, while explaining the downturn of remittance flows to emerging Asian economies, it all boils down to two words. OIL PRICES.

Consistent low oil prices and weak economic growth in the Gulf Cooperation Council (GCC) countries and the Russian Federation- the sources of almost 20% of global remittances- are taking a toll on remittance flows to South Asia and Central Asia.

The World Bank paints a pretty picture for the OPEC countries as it projects a stable increase in the crude oil prices. But, these figures should be treated with caution as other reputed analysts (e.g. Goldman Sachs) predict lower oil prices amid recent US shale surge. OPEC’s historic “November Deal- to curb oil production to pump up prices” had a sizeable impact on the market this year. But, players outside of the deal often disrupt the equilibrium- USA, Libya, Nigeria etc. to name a few.

GEO-POLITICAL BACKGROUND

Any country that exports labor force should do so maintaining a diversified range of migration destinations- to ensure a more sustainable and consistent flow of remittance, just like portfolio management- it reduces risks. Bangladesh has been able to accomplish this to some extent. With KSA, USA, UAE, Malaysia, Kuwait, UK and Oman leading the way, there are more than 30 countries from which Bangladesh receives a sizable amount of remittances.

When people talk about remittance in context of Bangladesh, they paint a picture of the GCC (or simply middle-Eastern) countries in their mind. Bangladesh may have a diversified portfolio of countries where it exports labor, but in the end the majority of the remittance earning comes from a single region- Arab states of the Persian Gulf (as seen in the tree map below).

These states together account for roughly 60% of Bangladesh’s remittance inflows. Unrest in the Middle East raises acute concern among the Bangladeshi people as millions of them depend on their family member(s) working abroad. The recent rows between Saudi Arabia and Qatar has raised a lot of concerns- the first and ninth most important (FY 15/16) remittance sources for Bangladesh.

The remittance money that Bangladesh receives from KSA is almost 7 times the amount it receives from Qatar. But in 2015, more Bangladeshis went to Qatar than they did to Saudi Arabia- mainly due to ongoing infrastructure projects ahead of the 2022 World Cup that will be hosted by Doha. Due to this reason, remittances from Qatar has remained steady or on the increase even in this time, when the global remittances had been decreasing.

KSA has been imposing restrictions on Qatar- urging its allies to weaken ties with Qatar as well. So, if Bangladesh is put in a diplomatic “with us or against us” situation by the Saudis- it’ll be facing a very difficult problem.

BOOSTING BANGLADESH’S ECONOMY

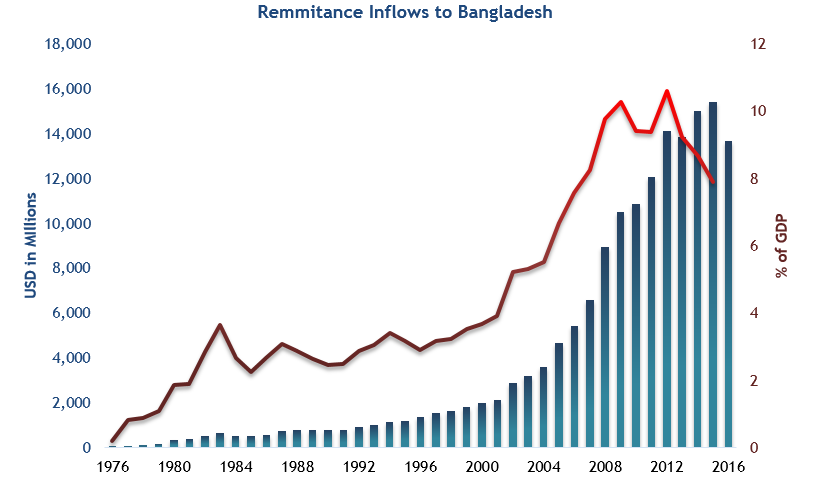

Since Bangladesh’s reception, emigrant workers have contributed a lot in jumpstarting the country’s economy- especially in the rural scene.

With the turn of the millennium, the labor export business boomed- and so did the remittance inflow. Gradually it became an instrumental part of Bangladesh’s economy. For the last decade or so, remittance has accounted for roughly eight percent of Bangladesh’s GDP.

While some economists argue that remittance is often bad for a country’s long-term growth, none can deny the effectiveness of it in reducing poverty. In developing nations, recipient households generally have higher levels of consumer spending and lower incidences of extreme poverty than their counterparts who do not receive remittances. Recipient families are also more likely to spend on education, and healthcare. The consumptive expenses of recipient households positively impact, via multiplier effects, the labor force market and incomes of non- recipient households too. The reason why remittance is such a powerful anti-poverty force in developing countries is that- unlike other publicly funded social safety nets, remittance recipients can identify their own greatest needs and can allocate the remittance income accordingly.

LINGERING FEAR

Recent trend of decreasing remittances has stirred up a lot of people- apart from RMG export, remittance has been the next most cherished thing by the people of Bangladesh. In the recipient families, a sense of dependency has developed on their relative who toils in a foreign land. The adverse effect of it has been the relatively lax attitude among them to be financially productive. Which means that, in the same way that remittances boost the economy via multiplier effects, a sudden fall might also cause a chain reaction of economic misfortunes.

The government needs to implement failsafe measures to minimize further deterioration. Monetary policies and immigration policies need to be amended and implemented to provide a stable remittance flow- because the country is not yet ready to move on from the remittances that it has been enjoying for the past two decades.

Author

Salman Zamal is a Junior Associate at LightCastle Partners. For further information, please reach out here: [email protected]

Bangladesh Bank. (n.d.). Retrieved from Bangladesh Bank: https://www.bb.org.bd/econdata/wageremitance.php

Europarl. (n.d.). Retrieved from Europarl: http://www.europarl.europa.eu/RegData/etudes/etudes/join/2014/433786/EXPO-DEVE_ET(2014)433786_EN.pdf

Trading Economics. (n.d.). Retrieved from Trading Economics: https://tradingeconomics.com/bangladesh/forecast

World Bank. (n.d.). Retrieved from World Bank: http://pubdocs.worldbank.org/en/662641493046964412/CMO-April-2017-Forecasts.pdf

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights

![Mitigating Risks for Matarbari DSP: Drawing Insights from Hambantota Port [Part 2]](https://www.lightcastlebd.com/wp-content/uploads/2024/07/IMG_0612-1024x682-1.jpg)