GET IN TOUCH

- Please wait...

The Monetary Policy Statement for FY2023-24 highlights the urgent concern regarding the high non-performing loan ratio within the financial sector. This trend creates substantial risks for the financial system as a whole. The last Monetary Policy Statement for FY2022-23, released in January of the same year, also stressed the adverse impact of high NPL ratios on the financial sector’s stability [1].

The Monetary Policy Statements of the Bangladesh Bank define the monetary policy stance, which is intended to support government policies and programs to achieve faster inclusive economic growth and poverty reduction while maintaining price stability [2].

Classified loans refer to loans that have been arranged and categorised based on their quality and repayment status. The purpose of these regulations is to evaluate the financial condition of banks and other financial institutions and to ensure responsible banking practices [3]. These categories consist of:

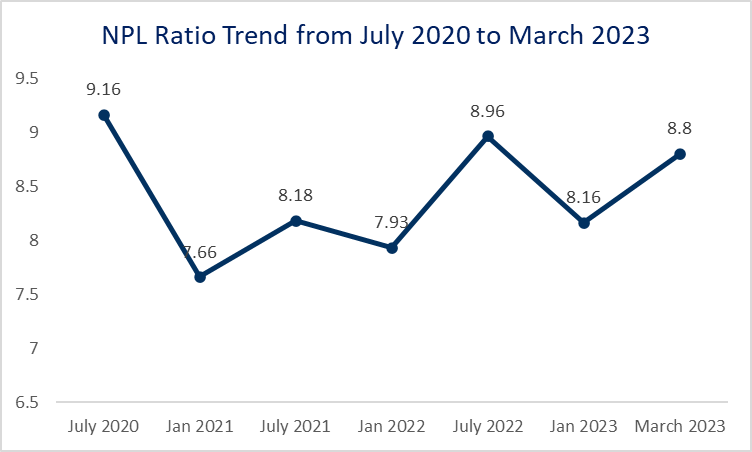

The NPL Ratio in Bangladesh was recorded at 8.8% in March 2023, amounting to BDT 14,963.46 billion (USD 136.92 billion), exhibiting an upward trend from the previous quarter’s ratio of 8.2%. The ratio attained its highest point in history, reaching 28.0% in March 2003, and its lowest recorded value of 6.1% in December 2011 [4].

This persistently high NPL ratio has implications beyond the financial sector, contributing to an increase in the exchange rate and a decline in foreign reserves. It diminishes investor confidence due to doubts regarding loan repayments, resulting in capital flight as foreign investors withdraw their investments [5]. This capital drain depreciates the local currency, raising the price of imported goods and services and leading to inflation.

The central bank may intervene to deplete foreign reserves to stabilise the exchange rate [6]. Such outcomes can set off a chain reaction, potentially leading to broader repercussions in the financial market.

This article provides a comprehensive analysis, deconstructing the various perspectives and insightful suggestions of experts who have critically investigated the phenomenon and the policy landscape.

Non-performing loans (NPLs) are loans for which the recipient has ceased or is unable to meet repayment commitments per the loan’s terms [7]. A significant accumulation of non-performing loans by banks or financial institutions can result in various negative outcomes, including economic instability, reduced lending capacity, higher interest rates, and reduced capital [8].

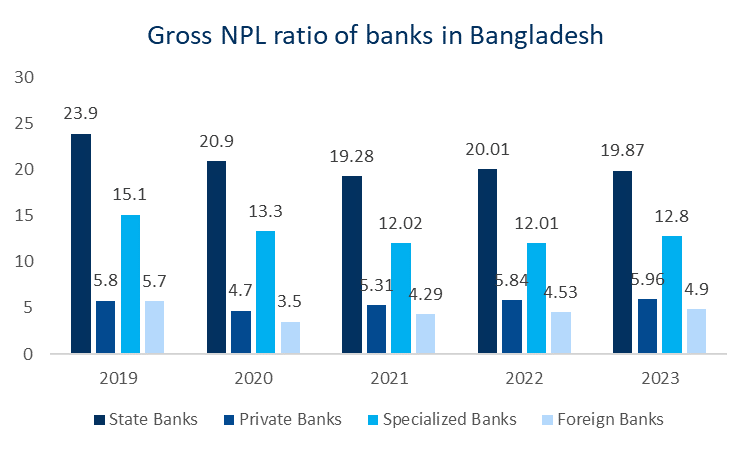

In developed nations, only 2% of a bank’s loans are permitted to be non-performing, whereas in Bangladesh, non-performing loans are currently at 8.8% [9]. The NPL ratio in our country has been marked as a major concern for both the financial sector and the economy for years. Yet, it persistently increases beyond the threshold level. A higher proportion of non-performing loans contributes to the financial sector going through turmoil.

In light of the crisis, the Bangladesh Bank has taken preventative measures to increase its control over financial institutions and major debtors.

While the recent changes in monetary policy show a willingness to address nonperforming loans, not everyone is convinced. According to former central bank governor Dr. Salehuddin Ahmed, no explicit orders have been made in recent monetary policy to decrease default loans [14]. In an interview, he emphasised the necessity for Bangladesh Bank to adopt a more firm approach, which entails halting financial support and foreign exchange assistance to banks incapable of successfully addressing non-performing loans.

Protracted legal procedures in money loan courts have contributed to the problem by leaving BDT 1,668.86 billion (USD 15.27 billion) in unpaid loans [15]. Dr AB Mirza Azizul Islam, a former financial adviser, has proposed limiting political influence in loan approvals and speeding up the conclusion of ongoing cases in the Artharin Adalat to resolve this problem.

The Centre for Policy Dialogue (CPD) has been advocating for establishing a banking commission for the better part of a decade, stressing the need for such a body to address pressing problems in the banking industry.

According to CPD, the primary function of such a commission is to conduct a thorough assessment of the state of the sector, ensure the public release of relevant data and information, investigate the origins of current problems, foresee potential roadblocks, pinpoint the responsible individuals and organisations in the event of a crisis, and offer specific suggestions for near-term and long-term administrative, regulatory, and structural improvements [16].

Former lead economist at the World Bank’s Dhaka office, Zahid Hussain, suggests that in recent years, rather than implementing effective measures, the central bank has taken several actions that have increased the number of loans in default. In addition, he expresses concern regarding the recent amendment to the Bank Company Act of 1991, which could threaten the financial stability of the banking industry [17].

The Executive Director of the Policy Research Institute of Bangladesh, Ahsan H. Mansur, shares a similar perspective, asserting that the central bank has taken no discernible steps to stem the development of default loans [17].

In conclusion, the NPL ratio in Bangladesh is an urgent matter that requires immediate attention. A multifaceted approach is necessary to solve this challenge effectively.

First, strict regulations should be implemented to prevent the accumulation of non-performing loans, emphasising strong corporate governance and prudent lending practices. Recovery of NPLs on time is crucial, necessitating proactive strategies, risk evaluation, and vigilant monitoring.

Effective monitoring across legal, physical, and monetary dimensions is essential for early detection and mitigation of NPLs. The resolution process can be streamlined by legal reforms, particularly the improvement of bankruptcy laws. Reducing vulnerabilities by rationalising the banking sector through consolidation and privatisation. Budgetary support should be provided to maintain essential services while establishing a national Asset Management Company (AMC) can facilitate the resolution of nonperforming loans [18].

Higher Non-Performing Loans can have far-reaching effects on an economy if they are not recovered substantially. Several Asian and European countries offer both failure and success stories in this regard.

As exemplified by the Republic of Korea during its post-1997 financial crisis, when nonperforming loans are not addressed, they can cause significant disruptions in the financial sector, threaten the stability of the entire economy, and pose systemic risks [18].

During its financial crisis, Greece’s consequences included reduced bank lending, increased financing costs for businesses and individuals, a contraction in economic growth, and severe strains on public finances [20].

In contrast, nations such as Malaysia and Thailand adopted proactive measures to recover from high NPL levels. In response to the Asian financial crisis, Malaysia, for instance, established state-run agencies such as Danaharta and Danamodal to address NPLs, thereby restoring confidence and decreasing NPL ratios.

Thailand utilised a similar strategy with agencies such as TAMC (Thai Asset Management Corporation) and the Corporate Debt Restructuring Advisory Committee, substantially exceeding market expectations for NPL resolution [18].

Indonesia also sets a great example of successful recovery. The country implemented robust NPL resolution frameworks and witnessed a significant reduction in NPL ratios, subsequently experiencing economic growth [21].

In conclusion, a comprehensive strategy encompassing prevention, recovery, structural reforms, and regulatory measures is necessary to address the high ratio of non-performing loans in Bangladesh’s banking sector.

The examples of success demonstrate that comprehensive NPL recovery measures, backed by effective legal frameworks and government interventions, can stabilise the financial sector, stimulate economic growth, and revive investor confidence.

Neglecting the path of NPL recovery can result in a prolonged economic recession, whereas successful NPL recovery can serve as a catalyst for economic revitalisation.

Amrin Hossain Tanisha, a Content Writer, with editorial support from Dipa Sultana, Senior Business Consultant & Project Manager at LightCastle Partners, has prepared the write-up. For further clarifications, contact here: [email protected].

1. Monetary Policy Statement, Bangladesh Bank

2. Monetary Policy Statement July December 2023, Bangladesh Bank

4. Higher NPL burden for banking sector, The Daily Star

6. Nonperforming Loans in Asia: Determinants and Macrofinancial Linkages, Asian Development Bank

7. Managing Nonperforming Loans in Bangladesh, Asian Development Bank

8. NPL and its impact on the banking sector of Bangladesh, The Financial Express

9. Financial Stability Report 2021, Bangladesh Bank

10. BB instructs state-owned banks to reduce non-performing loans, The Business Standard

11. Bangladesh: Requests for an Arrangement Under the Extended Fund Facility, Request for Arrangement Under the Extended Credit Facility, and Request for an Arrangement Under the Resilience and Sustainability Facility-Press Release; Staff Report; and Statement by the Executive Director for Bangladesh, IMF

12. NPL, another big foe to fight, The Business Standard

13. Financial Stability Report 2022, Bangladesh Bank

14. No clear direction on reducing banks’ NPLs, The Business Standard

15. NPL’s unstoppable rise, The Business Standard

16. The never-ending crisis in our banking sector, The Daily Star

17. Higher NPL burden for banking sector, The Daily Star

18. Managing Nonperforming Loans in Bangladesh, Asian Development Bank

19. Bank nonperforming loans to total gross loans (%), The World Bank

20. The Greek economic crisis and the banks

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights

![Mitigating Risks for Matarbari DSP: Drawing Insights from Hambantota Port [Part 2]](https://www.lightcastlebd.com/wp-content/uploads/2024/07/IMG_0612-1024x682-1.jpg)