GET IN TOUCH

- Please wait...

Sushmita Bala, a young, female entrepreneur, located in Botiaghata, Khulna, initiated her poultry enterprise in 2017 with 1,000 hens and adequate training. Albeit critical for growth, ever since her foray into micro-entrepreneurship, she never drew any loans or raised funds. However, due to the cyclone Amphan – causing massive destruction across the Southern belt of Bangladesh in 2020 – like several other SMEs, Sushmita’s firm had suffered an approximate loss of BDT 50,000. Feeling helpless, she’s now forced to look for traditional financing. But due to the structural challenges in the context of current SME financing practices in the country, she’s wondering if there’re any other viable options that can best serve her needs.

Sushmita’s story illustrates the difficulties all the micro and small entrepreneurs have to face when trying to raise funds. Two common issues include poor documentation and lack of financial literacy, both of which results in the undervaluation of business assets. According to the Bangladesh Bureau of Statistics, there are 7.8 million SMEs in Bangladesh, contributing 25% to GDP. It is the backbone of Bangladesh’s economy as it makes up more than 90% of all businesses which provide two out of three private-sector jobs. Because of the coronavirus situation, the entire SME sector has been exacerbated more than others. Recent statistics suggest, almost 68% of enterprises are at risk of shutting down & require immediate funding. While the Government has launched various stimulus packages amounting to BDT 200 billion, due to a number of limitations confronting the industry, the fund has not been able to be disbursed properly.

Theoretically speaking, there are two main ways of raising finance. One is debt financing by which one takes loans from an entity (such as banks) with an obligation to pay the principal amount with interest in due time; the other is equity finance, where one entity raises funds by selling shares of the enterprise. What differentiates between the two is that the debt financing does not inherit the business/operational risks versus equity ownership, which does consider. Typically in Bangladesh, funding is primarily done through debt financing. As a result, SMEs, particularly the rural entrepreneurs, lack the requisite know-how of the modalities associated with equity financing. Furthermore, the practice of equity financing is not well established in the country given all the connected risks with the funding itself.

Taking all these obstacles into account, LightCastle Partners has initiated a blended capital instrument with support from Oxfam Bangladesh in 2020. The goal of the fund is to promote equity investments to micro-entrepreneurs, allowing them to access growth capital on convenient terms. The first impact fund was launched with an initial investment size of BDT 1.5 million. This would be invested across 15 rural entrepreneurs in Khulna and Rajshahi with an aim to develop the regional promising firms’ capacities and to make them investment-ready for future growth.

To initiate equity funding, it is critical to assess the creditworthiness of the entrepreneurs before disbursing any funds. For this fund, we first collected initial data of 47 entrepreneurs across both the regions in collaboration with our local partners. The data that was collected centered around business financials, loan profile, client base, networks & legal documentation (such as NID, trade license & VAT license). After preliminary analysis, we shortlisted 27 candidates. The next step was to organize in-person interviews. However, due to the coronavirus-induced nation-wide lockdowns, we adopted online interviews as an alternative approach to conduct the interviews. Our local partners helped in organizing the logistics, allowing for successfully completing the interviews over 2 days. The interview process sought to have a deeper understanding of the entrepreneurs’ abilities, innovativeness, business model, financial returns, sustainability, gender inclusion, tech adaptability and enterprise size. Based on scoring, we were able to shortlist 24 final participants for the next step – the due diligence.

To further assess our final shortlisted candidates, we developed a tailor-made credit rating model, which would determine the top 15 entrepreneurs. So, we have developed an SME-friendly rubric model in line with the Bangladesh Bank scoring criteria guideline. Not only that, the rating model has also been designed through the lens of blended capital, which is essentially a mix of government/non-profit grants, equity investments and loans invested into a company. To learn more on how the concept works, read here.

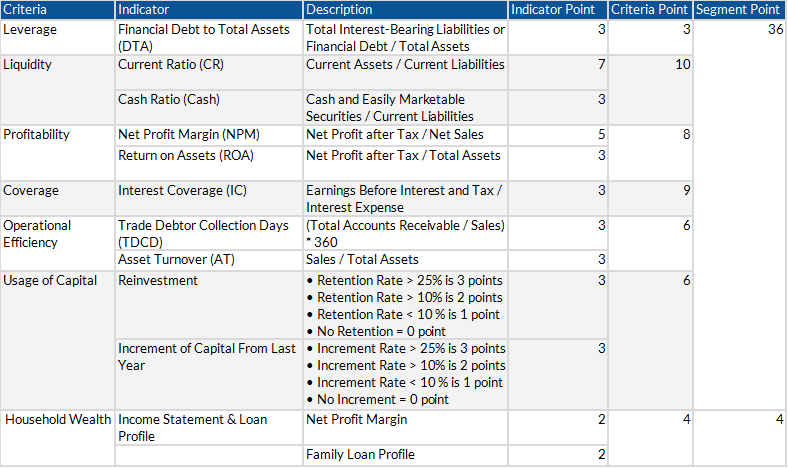

The rubric has two fundamental aspects: first, the quantitative analysis; second, the qualitative aspect. The tally for the quantitative segment was capped at 40 while for qualitative it was 25. A detailed questionnaire was formulated on capturing essential data points during the due diligence process. Two external local auditors were assigned to physically visit the enterprise locations for this exercise.

Once all the data was digitized and fit into the model, we were able to complete the requisite analysis. For the quantitative factors, we considered several ratios spanning leverage, liquidity, profitability, coverage, operational efficiency, earning quality & usage of capital. Apart from the enterprise’s hard quantitative data, we also accounted for the entrepreneurs’ household wealth, revenue and loan profile. This helped us to analyze other important numerical factors. Drawing on our experience of working with similar types of enterprises over the past few years, we assigned reasonable indicator and criteria points against each of the mentioned variables. All this enabled us to compare financial performances of each enterprise against another. The table below shows the quantitative rubric.

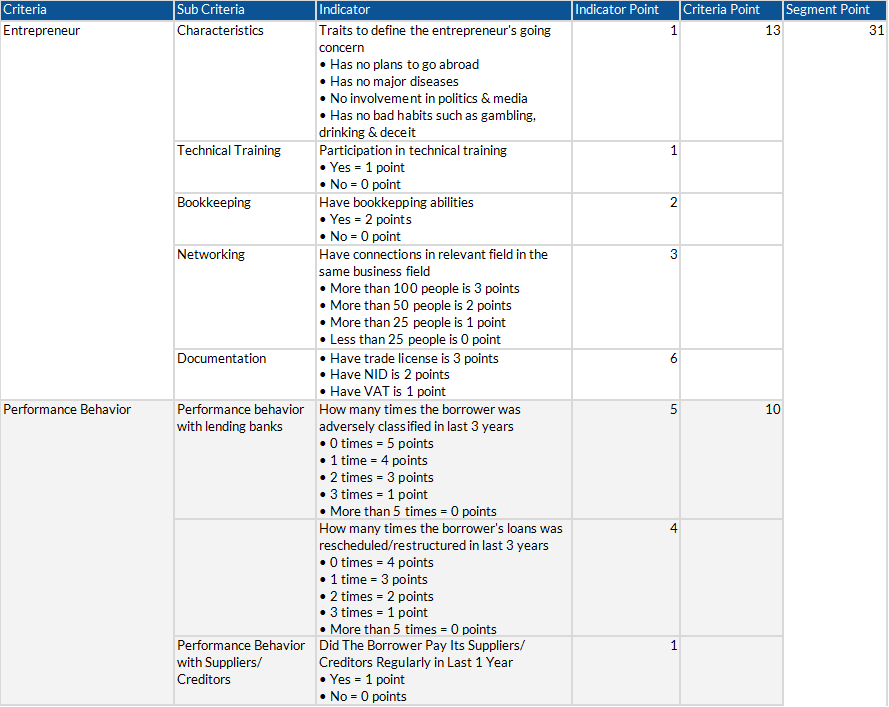

For the qualitative part, we included variables that assessed entrepreneurial characteristics, performance behavior, business and industry risk, and management issues. Entrepreneurial characteristics entailed various technical knowledge such as bookkeeping, networking, legal documentation and participation in training programs. Additional qualifying questions helped us further deep dive into the sustainable angle of the enterprises’ going concern. Performance behavior was measured in terms of the default rate on previous loans or credit to their suppliers. For business risk assessment, we considered the revenue growth changes year-on-year and the business age. And finally, for management risk, the overall experience of the entrepreneur was considered as a crucial indicator. Furthermore, in order to understand their commitment towards the enterprise, we collected information such as the amount of time they invest into their business, and degree of involvement with any other association or business. All these factors provided us with a complete picture of an entrepreneur’s qualitative performance.

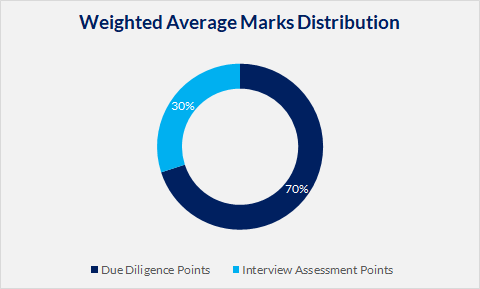

A weighted average model was developed to factor in combined scoring both the initial interviews and the due diligence. The breakdown is shown below:

Finally, by tying in scores from the different scoring grids, we fitted into one management reporting template, revealing the top 15 eligible for receiving the impact funding.

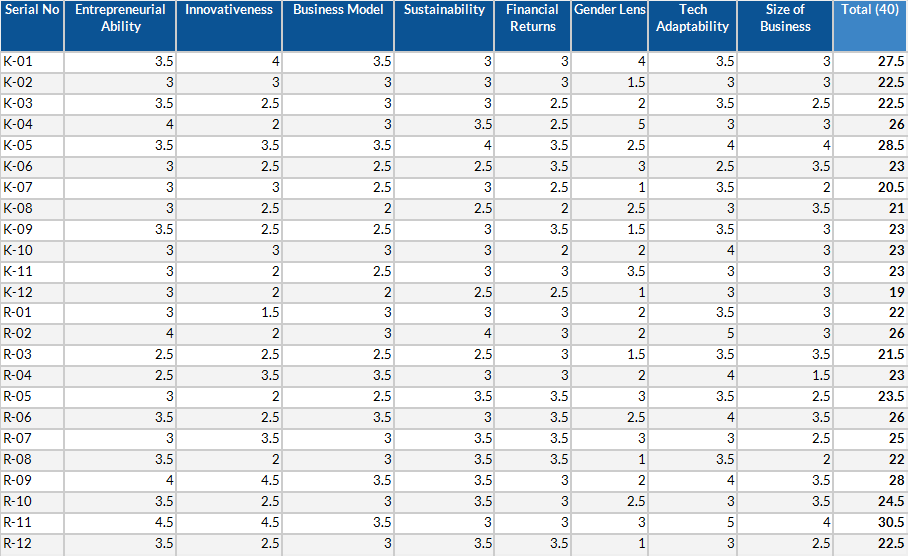

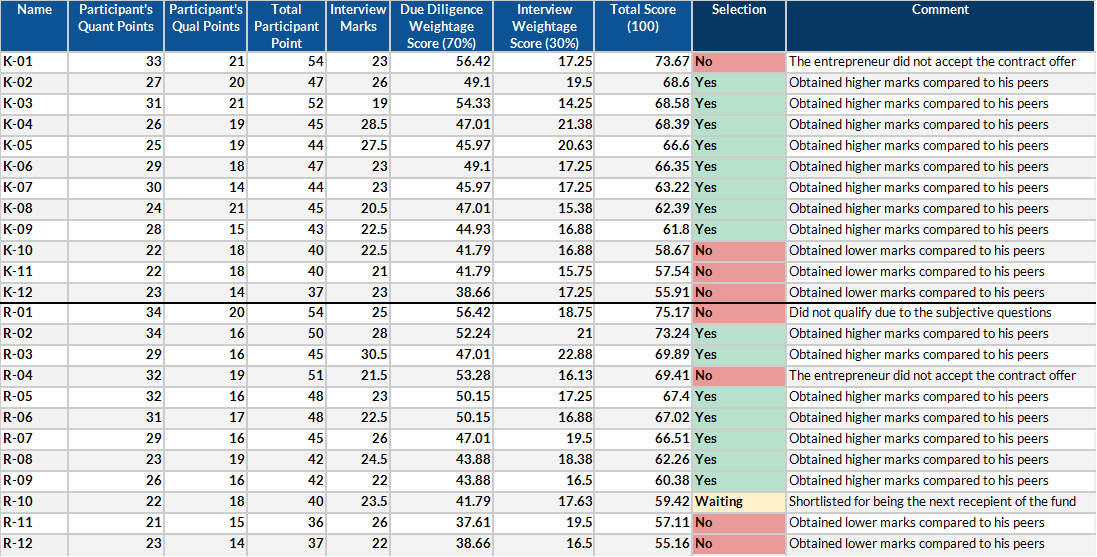

To give you an instance of how the individual scoring has been determined, let us consider K-01. He seemed to have obtained one of the highest scores among the 24 participants. By automating the model based on predetermined KPIs in the rubric, K-01 came out with a total of 54 points – 33 points and 21 points from quantitative and qualitative respectively. Since this score is attributable to the due diligence process, we converted 54 to 70%. Similarly, his interview score of 23 points (out of 40) was converted into 30%. Cumulatively, the model churned out 73.67 out of 100 as the final score for K-01. The below charts illustrate the final scoring of each of the 24 candidates from Khulna and Rajshahi. For Khulna, 9 out of 12 candidates obtained more than 60. Average score stood at 64.31, which is lower than the total average of 64.78. By comparison, the average score of Rajshahi arrived at 65.25. In terms of standard deviation, Khulna’s candidates had a lower differential of 5.31 compared to Rajshahi 6.36. Overall, Rajshahi fared better with regards to total scoring.

Developing innovative equity-linked instruments can bridge the gap in the blended capital landscape. And to do that effectively, tailor-made credit rating models hold the key. The credit rating model that we instituted is distinct and customized for SMEs like that of Sushmita’s. A systematic model has helped us to determine and inject growth capital into 15 solid enterprises. It is our hope that such models will encourage impact investors, foundations and the social sector to dare to think differently and embrace new models for development – creating pathways into the evolution of a sustainable, affordable and promising impact investment landscape in Bangladesh.

Ilham Hasan, Business Analyst, and Ivdad Ahmed Khan Mojlish, Director, at LightCastle Partners, have prepared the write-up. For further clarifications, contact here: [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights