Liberalize Trade to Accelerate Its Competitiveness: What Did the World Bank Say About the Trade Reform of Bangladesh

LightCastle Analytics Wing

August 16, 2023

The Bangladesh Development Update [1] is a twice-a-year report by the World Bank that highlights and analyzes the economic developments, prospects and policy challenges of Bangladesh. This article focuses on the April 2023 edition of the report, where trade reform and export diversification have been especially highlighted as an impetus to the growth and resilience of the Bangladesh economy.

This article gives a snapshot of the overall findings of the Chapter “Trade Reform in Bangladesh: An Urgent Agenda” of the mentioned report.

Introduction

Bangladesh has earned remarkable economic developments in the last five decades from starting as a basket-case economy in 1972 to becoming the 35th largest economy in the world in 2022.

Trade has been, so far, a reliable partner of Bangladesh in ensuring her continuous and robust economic growth, generating employment, and reducing poverty, with a current share of 34% in her GDP (2022, The World Bank). Besides, it is also important for ensuring a smooth ride toward achieving Upper-Middle Income status in 2031.

Openness in Trade and FDI has been an important accelerator of Bangladesh’s growth since the 1990s by surging the volume and value of exports. Various novel policy interventions, including trade and FDI reforms such as back-to-back Letters of Credit and the creation of new export processing zones, contributed to the growth in per-capita income over 1995-2004, as per the World Bank (2022). However, trade reforms have been slowed down in the past few years, and a significant lack of new policy innovations in this arena has reduced the contributions of trade and FDI to growth, during the period 2010-2019, as per the World Bank (2022). Hence, to facilitate the rebounding of the contribution, reforms like trade facilitation, service and FDI liberalization, tariff modernization, and the removal of non-tariff barriers can be consequential.

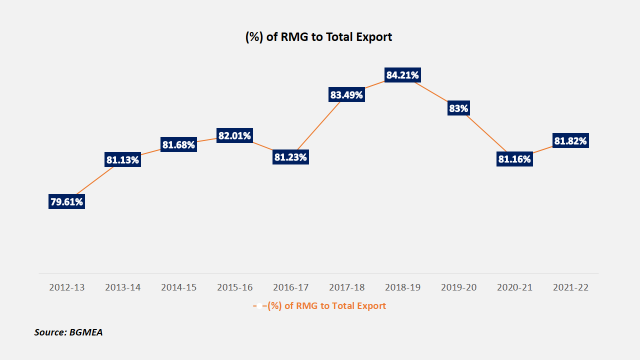

At present, Bangladesh’s export basket depends heavily on RMG, whose share in the export earnings in FY 2022 was 81.8%. [2].

Figure: (%) of RMG to Total Export of Bangladesh

And now, apparel is the only industry among the major exporting sectors in Bangladesh that has been able to retain growth in earnings. [3].

This lack of export diversification can be linked to Bangladesh’s extreme trade barriers, which question the workability of her inward-oriented growth model, a model that incentivizes domestic industries and import substitution behind trade barriers to foster development.

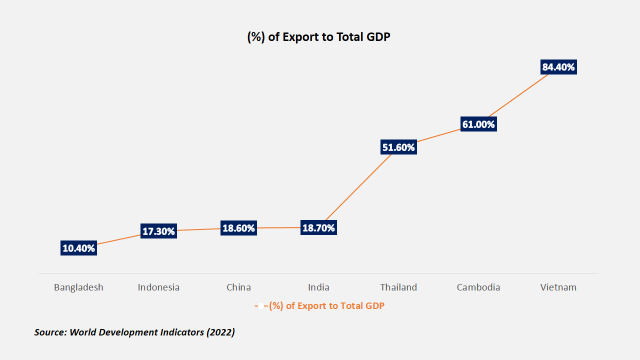

However, Bangladesh still has room for improvement to increase its share of exports in GDP, which is currently much lower than that of its similar trading counterparts, through implementing the necessary impactful reforms and liberalization.

Figure: (%) of Export to Total GDP of Bangladesh and her trading counterparts

The Attributes Confirming Bangladesh’s Eroding Trade Competitiveness

Bangladesh’s depleting trade competitiveness is not just a concept anymore but the attributes supporting the concept are very visible. The attributes identified by the World Bank, in support of this concept are as follows:

Downward trend in trade performance: In terms of both country’s historical performance and overall economic growth, there has been a downward trend in Bangladesh’s trade performance since 2011. The contribution of manufacturing exports to growth, on which the country heavily relies on, has been decreasing over the past five years. Besides, the share of goods and service trade to GDP has been decreasing since 2011, and the share has been much lower than that of the share of the countries like Thailand, Cambodia, Vietnam, Indonesia, etc.

High density of exports (81.82% in FY 2021-22) is concentrated in RMG: This concentration is also reflected in the number of export products and markets, where the number of export markets is still closer to that of India, China, Vietnam, Indonesia, etc. but the number of export products is significantly lower than the mentioned peer countries and almost 1/4th and 1/5th of the export products of India and China respectively. Besides, the contribution of good export to GDP was 9% as per 2021, which is much lower than the average 25%, for low and middle-income countries [1]

Share of intermediate and capital goods is declining in our diversified import basket: The share of these two categories in total imports stood at 32% in 2020, compared to 43% in 2005. Capital machinery, primary and intermediate goods in Bangladesh are mainly imported for setting up new plants, expanding industrial units, increasing production and developing Government infrastructure. Besides, World Bank Exporter Dynamics Database for 2015-2016, shows that Bangladesh’s export products have high import contents and this declining share of intermediate and capital goods in a way hampers the final goods production output.

Higher reliance on Remittance for mitigating the risk of FX earnings: This reliance is much higher than that of the peers like Vietnam, India, Malaysia, Thailand, etc. and is lower than only the Philippines and Nepal, to run a modest current account surplus and to balance out the loss from eroding trade performance

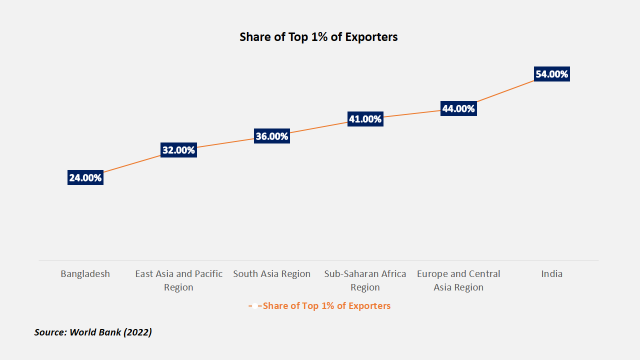

The share of superstar exporters is low compared to their peers: The firms that account for a very large share of exports are export superstars. These top firms with their high efficiency level and large-scale business fetch a comparative advantage in the global market for the country and its export products.

Figure: Share of Top 1% of Exporters of Bangladesh and other Regions

Lower survival rate of new entrants: The survival rate of new exporters (28%) is higher compared to regions like Sub-Saharan Africa (22%), Middle East and North Africa (27%), etc. but lower compared to that of India (36%) and regions like South Asia (30%), East Asia and Pacific (37%) and Europe and Central Asia (34%), etc. Survival of new exporters highly depends on proper policy support through reduction of import duties and VATs, access to necessary finance and smooth and enhanced participation in GVCs and Research and Development.

Key Reasons for Bangladesh’s Eroding Trade Competitiveness

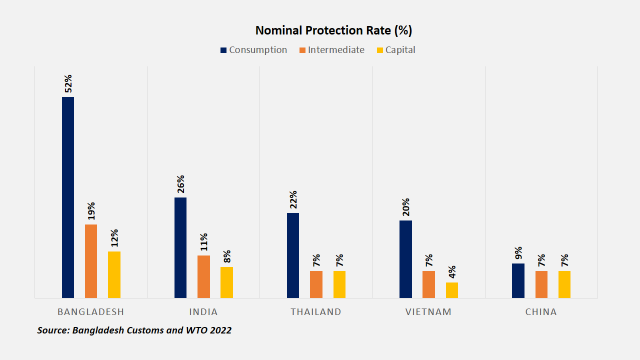

Domestic market-oriented industrialization focused policies havemade Bangladesh a protective trade regime: Para tariffs such as regulatory and supplementary duties in Bangladesh, increase the complexity of tariff structure and increase the number of tariff rates from 6 to 50, doubling the average nominal protection rate of import from 14.7% to 28.8% and thus results in the highest tariff escalation among the comparators mainly in terms of the difference in nominal protection rate for consumer and intermediate goods. This highly protective regime decreases the export survival probabilities of exporters and Global Value Chain (GVC) participants, whose different stages of production are dependent on the imported goods

Figure: Nominal Protection Rate of Import of Bangladesh and her similar trading counterparts

High degree of protection for domestic (import substituting) industries at the expense of emerging and potential export industries: Trade policy in Bangladesh, except for the duty free regime provided to the RMG sector, highly incentivized import substitution and deepens the anti-export bias. The average nominal protection of final goods is 5 to 10 times higher than that of the intermediate goods for sectors like transport, equipment and textiles

Non-Tariff Barriers are also significantly higher than comparators: Non Tariff Barriers like sanitary and phytosanitary requirements, pre-shipment measures, licensing requirements, price control measures increase Bangladesh’s trade restrictiveness and deter firm’s trade competitiveness. The percentage of non-tariff barriers in Bangladesh is much higher than that of India, Indonesia, Thailand, China and is only lower than that of Cambodia

Rising Trade Cost due to inefficient border processes: Time required to complete border and documentary compliance by the exporters of Bangladesh causes delay of about 300 hours, which is almost 10 times that of China’s and 5 times that of India’s practices. Besides, the implementation rate of WTO Trade Facilitation Agreement to ease the international trade facilities in Bangladesh is very low

Hamper in service trades due to Higher Ad Valorem Equivalents (AVEs) and less efficient service trade policies: AVEs in the service sector are high compared to tariff rates in the goods sector. Though AVEs are highest in the telecom sector (52% in average), it is much lower in sectors like finance ( 18% in average), transport (22% in average) and distribution (26% in average). But, Bangladesh has less attractive policies in service sector comparative to others, especially in the transport and telecom sector, to take advantage of the lower AVEs

Other Restrictions: Bangladesh posing significantrestrictions in visa processing, land acquisition and data transfer also hinders the competitiveness of trade

LDC Graduation: A Further Blow to Bangladesh’s Trade Competitiveness

Bangladesh’s graduation from the Least Development Country Status in 2026, will have a significant impact on her current state of trade competitiveness. [4]

Bangladesh will lose the duty-free and quota-free market access as a LDC: This LDC graduation will trigger another 3-year term of transition period after which Bangladesh is set to lose the duty-free and quota- free market access under Everything But Arms initiative. Almost half of Bangladesh’s exports go to the EU market, including the United Kingdom, which accounts for 60% of the trade. And this export is expected to shrink by 28%- 30% after LDC Graduation. [5].

Hike in Export Tariff: Bangladesh will face a tariff increase of 10% for most clothing products. The country will face around 16% to 18% charges for 10 of the top 12 products in Canada and around 8% to 11% in the Japanese Market. However, the increase in tariff will be lower for exports to the United States, Australia and India and Bangladesh will be getting preferential trade benefits from the Chinese Market under Asia Pacific Trade Agreement (APTA)

Expected Reduction in RMG Export Volume: It is the clothing sector that is going to face the bulk reduction in export volume due to LDC graduation. Share of initial exports of clothing to Canada (42.8%), Japan (32.2%) and the Republic of Korea (32.3%) will decrease significantly. As per a report by UNCTAD, Bangladesh may lose 14.28% or US$ 5.73 billion worth of export earnings after LDC graduation.[6].

However, Bangladesh is trying to negotiate a special arrangement with the EU to access the Generalised Scheme of Preferences Plus (GSP+),that would retain the tariff preference in condition of commitment to strong sustainability standards in terms of worker’s rights, climate smart practices etc.

Key Reforms that will result in a Positive Trade Outlook

Reduce import protection schemes to improve export competitiveness: Import protection focused policy, could be a path towards the middle income trap, a situation where the middle income country is failing its transition to high-income countries due to decreasing competitiveness . Policies that help exporters to properly access the imported intermediate goods can improve exporters performance, make export globally competitive and help in proper integration in GVCs by moving up the technology ladder. Otherwise, protecting domestic market and promoting export just doesn’t go together

Modernization of the Tariff Regime to improve the export diversification: The goal highlighted in Bangladesh’s 8th Five-Year Plan to reduce the nominal protection rate by 3-5% every year until 2025 needs to be implemented properly and a new National Tariff Policy should be laid out to promote investments and improve competitiveness. A low and uniform tariff rate for all kinds of products should be worked out

Tariff Reforms and Tax Rationalization should run concurrently to balance out any revenue losses: Reduction of tariffs in Bangladesh to the level of other middle income countries like China, India, or Vietnam, would result in tariff revenue loss between 18% and 41%. And hence improving the tax collection and widening the tax net is essential to compensate for the losses of existing tariffs and para tariffs, as Bangladesh total revenue collection amounted to only 8.27% of the GDP in FY 23-24 (until Feb’23), which was one of the lowest in the world

Role of Trade Liberalization in Boosting Bangladesh’s Trade Performance

Unilateral Liberalization brings the highest gains for Bangladesh: Analysis by World Bank shows that Unilateral Liberalization, where Government allows its nationals to trade freely with the foreigners regardless of the policies pursued by the Foreign Governments, of trade and barriers brings the highest gains for Bangladesh by boosting her GDP, investment and exports by 14.28%, 20% and 63.2% respectively. This would significantly benefit the apparel, retail trade and transportation sector by decreasing the cost of trade and give better access to quality imported inputs and in return will increase export quality, output and competitiveness

Bangladesh better-off with Unilateral Liberalization to Bilateral Liberalization: However, analysis of the gains from bilateral liberalization, where Government of two nations negotiates different policies to increase the trade volume between each other, with India and EU show that the percentage of gains is lower than that of unilateral gains, but bilateral liberalization along with trade tariff, FDI, Non- Trade Barriers will further boost the share of gains

Bilateral Trade Agreements with India boosting Exports by higher percentage than that of Europe: Bilateral trade agreements with India and Europe can boost Bangladesh’s export by 3.9% and 1.4% respectively, and this higher weight towards agreement with India can be estimated from the preferential trade benefits already existing with Europe. Bilateral trade agreements are expected to boost inter country trade and can contribute to higher value added manufacturing and services

Preferential Liberalization works better for Bangladesh over Multilateral Liberalization and should strengthen Regional Integration: In comparison with different similar south asia and south east asian countries, World Bank analysis show that Bangladesh is better off in gaining trade benefits upon preferential liberalization rather than multilateral liberalization. Multilateral trade liberalization, where all trade related decisions contributes to reducing tariff and non-tariff barriers to trade to all countries or atleast the majority of them, brings benefits for countries such as China, Indonesia, Myanmar, Singapore etc, but preferential liberalization, where a country gives a single country or a large group of countries some preferential trade benefits over others, brings benefits for Bangladesh, India and Pakistan. And, hence liberalizing the trade policies between Bangladesh and South Asian and South-East Asian countries will help to boost our economy

Conclusion

As Bangladesh aspires to be an upper-middle income country by 2031, it needs to raise its GNI per capita to a minimum $4,256 from its current GNI per capita $2,793, as of July, 2022 and also needs to achieve an annual average GDP growth rate of 8% as per 8th Five-Year Plan [7]. Therefore, for carving a more successful story in the Global Value Chain by Bangladesh, diversifying the export basket and improving trade competitiveness is an urgent call for holding up the country’s downward trade performance.

Author

Adiba Haque Ahona, Trainee Consultant at LightCastle Partners, has prepared this write-up.

At LightCastle, we take a systemic and data-driven approach to create opportunities for growth and impact. We are an international management consulting firm which creates systemic and data-driven opportunities for growth and impact in emerging markets. By collaborating with development partners and leveraging the power of the private sector, we strive to boost economies, inspire businesses, and change lives at scale.

![Mitigating Risks for Matarbari DSP: Drawing Insights from Hambantota Port [Part 2]](https://www.lightcastlebd.com/wp-content/uploads/2024/07/IMG_0612-1024x682-1.jpg)