GET IN TOUCH

- Please wait...

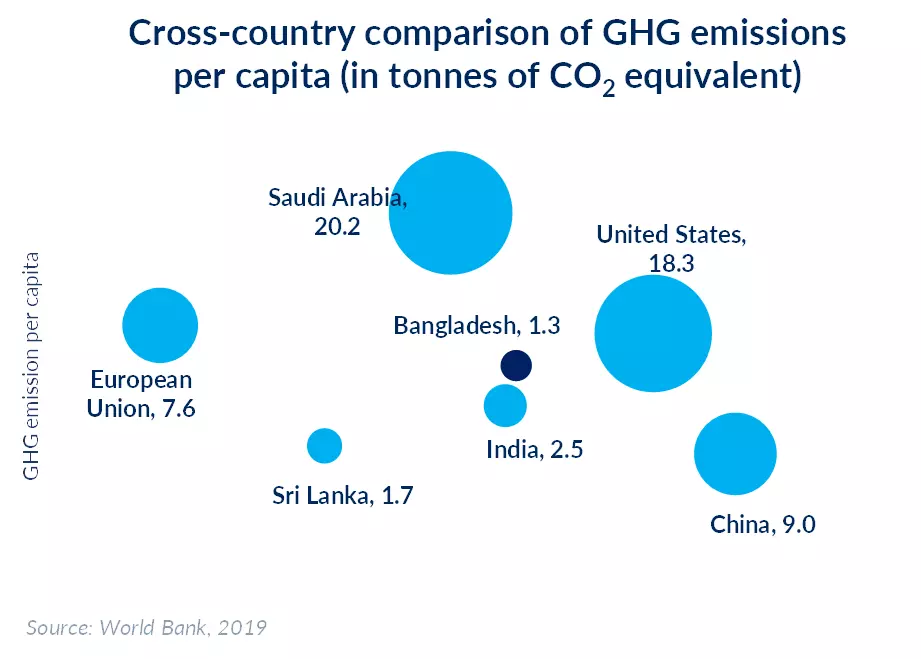

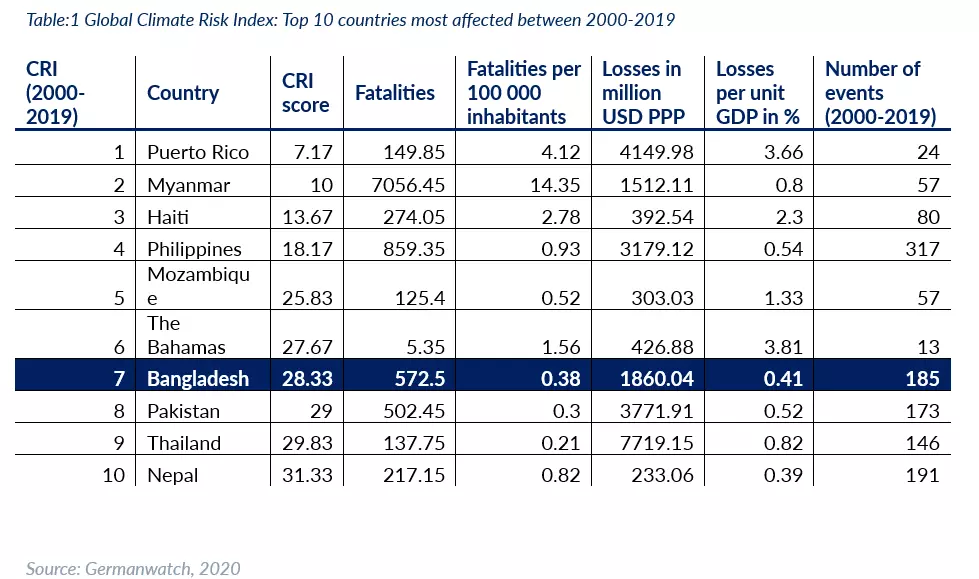

Bangladesh has consistently achieved an impressive average annual Gross Domestic Product (GDP) growth rate above the 6% mark leading up to the pandemic. Yet, in the long term, we risk losing 2% of annual GDP to rising sea levels by 2050 and 9% by the end of the century [1]. Despite consistently being one of the lowest emitters of greenhouse gases with a 0.4% contribution [2], Bangladesh has ranked seventh in the Global Climate Risk Index’s analysis of countries most affected by the impact of weather-related loss events [3].

Based on this vulnerability, Bangladesh has been a strong advocate for a unified compensatory fund to facilitate mitigation measures and pertinent climate interventions to sustain its economic growth during the last few Conferences of Parties (COPs) – a series of United Nations (UN) conferences assessing progress in dealing with climate change dating back to 1995.

Around the world, the most vulnerable developing countries are categorised into four sub-groups: Alliance of Small Island States, Independent Alliance of Latin America and the Caribbean, the Africa Group, and Least Developed Countries, with Bangladesh currently belonging to the fourth sub-group. Climate negotiations such as the COP use this categorisation to assess the impact and determine the flow of funds. COP27 concluded in November 2022 with the historic achievement of a Loss and Damage fund for developing countries hit hardest by climate change [4]. Additionally, Bangladesh was also named as one of the first recipients of the Global Shield – a German-led adaptation fund providing access to additional financing for recovery from natural disasters and climate shocks [5].

Moreover, in 2022, the Green Climate Fund (GCF) in collaboration with Bangladesh’s Infrastructure Development Company Limited (IDCOL) began implementing a USD 340.5 million project promoting private sector investment through the large-scale adoption of energy-saving technologies and equipment for the local textile and readymade garment (RMG) sectors. USD 256 million of this came in the form of a loan from GCF and the remainder is being co-financed [6].

In November 2026, Bangladesh is scheduled to graduate from the Least Developed Country (LDC) category. After 46 years of being enlisted in the category, the nation has finally been given the go-ahead to graduate after meeting all three of the requirements as determined by the UN’s Committee for Development Policy (CDP) and being evaluated for the second time in February 2021. This transition will bring with it both opportunities and challenges for the nation.

Bangladesh, being one of the most climate-vulnerable nations, will be losing out on Official Development Assistance (ODA) and specialised financing opportunities necessary to address challenges such as the climate crisis. Till date, Bangladesh has received a significant amount of foreign financial support for building climate resilience from dedicated climate finance facilities such as the Global Environment Facility (GEF) Trust Fund, GCF, Pilot Program for Climate Resilience (PPCR), and Adaptation (AF) among others. With their numerous programs, instruments, and financing options for combating climate change, multilateral development banks like the World Bank and the Asian Development Bank (ADB) have also played a crucial role as financiers.

The Government of Bangladesh (GoB) has also taken several initiatives to combat the impact of climate change. Bangladesh was one of the first LDCs to create a National Adaptation Plan of Action (NAPA), which outlines activities for addressing the country’s immediate needs for climate change adaptation and it is comprised of four pillars:

In addition, in 2009, the Bangladesh Climate Change Strategy and Action Plan (BCCSAP) was drafted which outlined 44 programs of action within six thematic areas:

Some other notable initiatives by GoB also includes Climate Change Trust Act 2010, Bangladesh Delta Plan 2100 (BDP 2100), a ten-year Implementation Roadmap for the Nationally Determined Contribution (NDCs) for 2016-2025 – prepared to manage growing emissions without compromising economic development, Perspective Plan (2021-2041) and 8th Five-year Plan (2021-2025). [7]

Despite all the notable policies and initiatives, Bangladesh has lacked in terms of efficient implementation of the existing policies and programs. It will be crucial to improve the legislative and institutional capacity by empowering local governments to plan, design, and implement climate programs efficiently. Given the urgency, scale, and complexity, partnerships among NGOs and Civil Society will be instrumental.

In addition, climate finance from the private sector has the potential to rise around 0.2% of GDP up to $ 1 Bn by 2025. [20] Therefore, increased foreign and private sector involvement such as climate-smart agriculture and the use of renewable energy will also play a major role in mitigating climate impacts.

Furthermore, along with government initiatives, private, and non-banking financial institutions are also assisting in the development of low-emission and climate-friendly infrastructure around the country. Bangladesh Bank has also actively pushed for the establishment of a green economy. In 2011, the bank started a comprehensive green banking initiative to support environmentally responsible financing. As a part of this drive, Bangladesh Bank commenced providing commercial banks and other financial institutions with incentive-based programs, such as financing facilities at a low-interest rate for lending to green projects.

During that year around 838 million funds were allocated to segments such as solar irrigation pump, solar home system, biogas plant, and solar PV module assembling plant, among others. [19] In 2016, the $200 million Green Transformation Fund was introduced by Bangladesh Bank and the same year, the country’s banking and non-banking financial institutions were instructed to set aside 10% of the Corporate Social Responsibility (CSR) funds for a Climate Risk Fund. To offer direction and laws for greening efforts to be done by banks and financial institutions in Bangladesh, the Sustainable Finance Policy for Banks and Financial Institutions was developed based on these lessons and best practices.

Climate change poses a significant threat to sustainable growth in Bangladesh and remains a challenge that requires a multifaceted approach. To that extent, the green industry is a concept coined by the United Nations Industrial Development Organization (UNIDO) that contextualises sustainable industrial development through green public investments and policy initiatives that encourage responsible private investments [8].

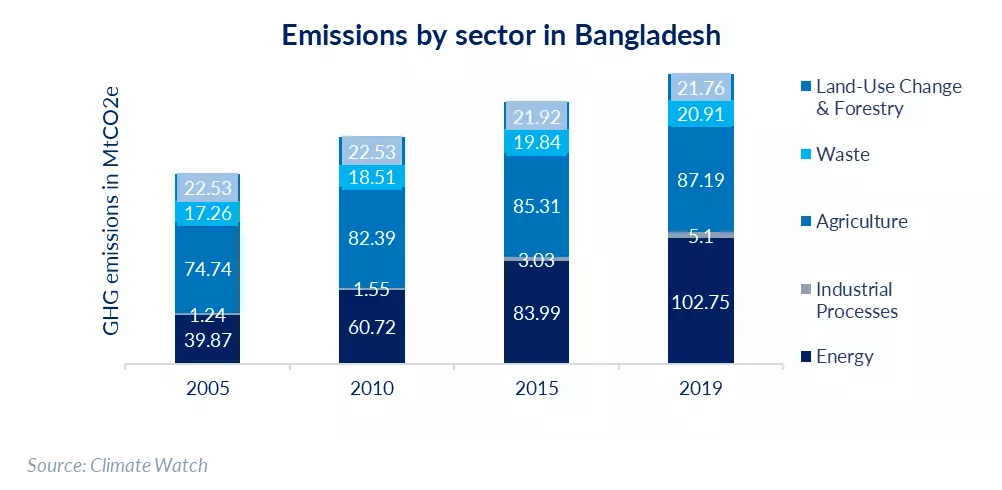

The Nationally Determined Contributions (NDC) prepared ahead of COP26 in 2021 exemplified the implementation of the green industry in Bangladesh. The energy sector in Bangladesh is the largest sectoral contributor to emissions with power, transport, and industry as its three major sub-sectors. The NDC outlined an unconditional 6.7% reduction in greenhouse gas (GHG) emissions.

In industry, the measures to achieve this entail a 10% higher energy efficiency through measures according to the Energy Efficiency and Conservation Master Plan (EECMP). In contrast, external financial and technological support could mean a 15.1% reduction in GHG emissions. This conditional commitment to a greater reduction would involve a 20% increase in energy efficiency in industry, as well as the promotion of green industry and carbon financing [9].

The urgency to develop resilience and the potential of green financing underpin a changing landscape within the country. Progress in the industry has already been underway for some time. The Bangladeshi apparel sector currently has 9 of the world’s top 10 green factories, a cumulative 186 factories with Leadership in Energy and Environmental Design (LEED) certificates and another 500 factories in the certification pipeline [10]. The Bangladesh Garments Manufacturers and Exporters Association (BGMEA) reports that these green factories are expected to help reduce energy and water use by 40%. BGMEA has also pledged a 30% reduction in GHG emissions by 2030 and committed to a safer working environment for employees through improved design [11].

Prior to the pandemic, the shift to green factories helped apparel manufacturers move away from a deserved yet rather critical sweatshop image following the Rana Plaza incident in 2013. More recently in the context of global economic turmoil, manufacturers believe these certifications can enhance competitive advantage in a time of decreasing orders by boosting business confidence in major export destination markets. The growing number of factories committed to a sustainable, energy-efficient, and environmentally friendly apparel industry has also been theorized to provide a vantage ground in international green deals.

The government also plans to set up 100 green economic zones by 2030, 30 of which are currently under development [12]. The Bangladeshi Economic Zone Authority (BEZA) says these zones will take comprehensive approaches to managing waste as opposed to contamination by individual businesses, as well as provide incentives to use clean energy from biomass. One such example is the Japanese economic zone in Narayanganj, which will have a central facility for processing liquid waste, afforestation measures and solar rooftop panels.

Side by side, the Sirajganj economic zone plans to allocate only 60% of its land to factories, envisioning green infrastructures such as a solar panel park and rainwater harvesting system for the remaining area [13]. The overarching theme of these zones is to improve the ease of doing business in Bangladesh and promote an inflow of foreign investments. Facilitating local operations of foreign subsidiaries in economic zones can enable the transfer of knowledge and expertise, as well as provide access to better technologies. However, inadequate profit repatriation systems for investors remain a commonly reported barrier. Moreover, these economic zones raise concerns about land use and food security, as Bangladesh is currently losing cropland at a conversion rate of 0.7% annually.

Under the wider label of sustainable bonds, green bonds are fixed-income instruments that are designed to fund climate and environmental projects. Globally the green bond market was valued at USD 2 trillion at the end of Q3, 2022 [15].

Regionally, Indonesia launched a Green Bond and Green Sukuk Initiative in 2018 to support its aims for GHG emission reductions. The first sovereign green sukuk (Islamic bond) issuance was worth USD 1.25 billion and attracted investors not only within Indonesia and the Islamic market, but also from wider Asia, the European Union (EU) and the United States of America (USA). Proceeds from this issuance were earmarked for green projects that also met Islamic criteria [16].

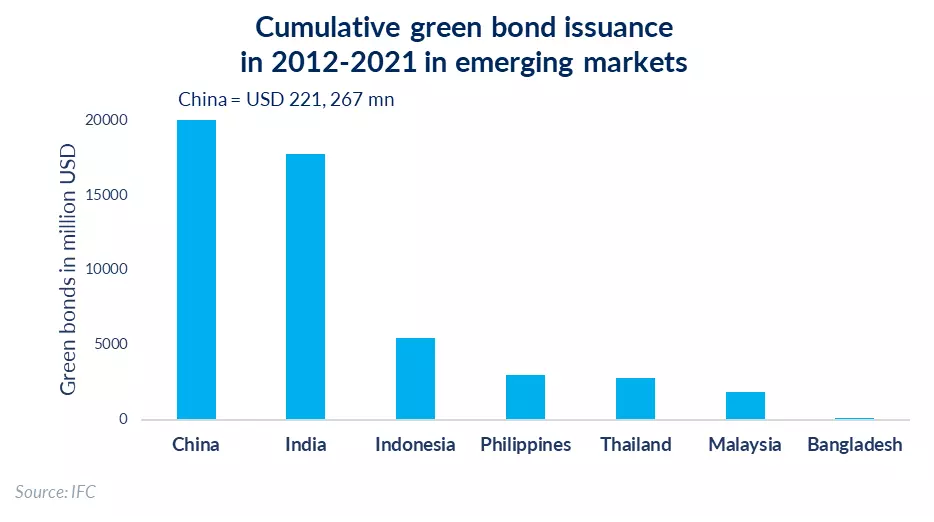

At present, the bond market in Bangladesh is small and primarily comprised of government bonds. In April 2021, the government permitted the local NGO Sajida Foundation to raise USD 9.3 million from the capital market by issuing the first green bonds in Bangladesh to increase the outreach of their microfinance program [17]. Bangladesh Bank has also recently circulated its guideline on green bonds for banks and financial institutions.

Currently, there are a limited number of commercially viable green projects [18]. Developing eligible, scalable, and profitable projects that engage both international and domestic private sector financing paves the way forward for sustainable economic growth.

In addition, according to the conditions set by International Monetary Fund (IMF), Bangladesh has to implement activities and programs in the next budget to deal with climate risks as per the loan conditions. Recently, Bangladesh has bagged a $4.7 billion IMF loan and $1.3 billion of this amount came from the Resilience and Sustainability Facility (RSF). Bangladesh is among the first Asian countries to receive this fund to meet the climate change challenges of the country.

Renewable energy sources (RE) have a lot of potential, yet they only make up 1% of Bangladesh’s total energy supply [21]. This subpar performance can be attributed to a lack of technology, poor institutional and regulatory frameworks, and weak policies and incentives.

Although Bangladesh Bank has developed green banking guidelines, the underdeveloped equity and bond markets, the under capacity of banks and financial institutions, and the lack of a clear understanding of the risks and returns of green projects – all limits the expected growth of green projects in Bangladesh.

Case in point, a notable example of a public-private partnership in green financing is IDCOL’s solar homes program in Bangladesh. The failure of the program’s commercialization, poor financial governance, the absence of a national policy oversight body, the uncoordinated grid electricity expansion, the lack of coordination among the relevant agencies, and the enormous amount owed to customers have put this program on the verge of being abandoned.

However, this case provides evidence that renewable energy within the power sector can be explored further by replicating similar initiatives of rooftop solar, setting up solar plants but by ensuring proper reforms such as financing opportunities based on capital and operational expenditures.

Furthermore, by 2030, under the ‘business as usual’ scenario, the transportation sector will be responsible for 8.86% of all GHG emissions in Bangladesh, according to the country’s updated Nationally Determined Contributions (NDC). The country’s energy sector emissions rank it as the third-largest sub-sector. Thus, Bangladesh needs to consider directing more of its attention toward the switch to electric vehicles (EVs).

It’s high time that Bangladesh starts developing the EV charging infrastructure before EVs are widely adopted. Only 14 solar-powered EV charging stations with a combined 282 kW capacity exist at the moment. Most of the current EVs are run using residential charging setups. In the current CNG and fuel stations, EV charging stations could be added.

Side by side, to encourage EV adoption in Bangladesh, significant financial incentives are required. The government can formulate favorable policies to promote wide-scale EV deployment, expedite the import and encourage domestic manufacturing and assembling of EVs through tax holidays, and interest waivers on loans. The price difference with conventional automobiles may also be closed with the aid of purchase incentives and registration tax exemptions.

Besides, banks could be encouraged to increase lending to the EV sector by designating it as a priority sector for lending. Due to the EVs’ ambiguous resale value, the government, in collaboration with multilateral, can implement risk-sharing structures to cover potential losses associated with EV financing.

Over the past few years, Bangladesh has excelled in the growth of the startup ecosystem. In the first half of 2022, Bangladeshi startups raised over $90Mn. [22] This demonstrates that our local talent can develop viable strategies to draw in foreign investment, and it also presents us with a big potential to transition towards a greener economy with innovative and smart solutions.

Future-focused investors from around the world are now more interested than ever in Bangladesh. It’s past time for our ecosystem to work together and in the near future, we’ll be able to become bigger and better by expanding the opportunities’ inclusivity and collaboration.

As the nation strives to become a middle-income country by 2030, innovation will be the driving force behind sustainable and inclusive development and technology innovators/startups such as SOLshare, iFarmers, bKash, and others will play a critical role in overcoming the nation’s various climate challenges.

A concerning takeaway from COP27 was that the 1.5ºC controlled warming target may likely no longer be realistic. Despite global reduction or net-zero commitments and the increasing implementation and availability of financing, GHG emissions are on a trajectory that could lead to a temperature rise between 1.7ºC and 2.4ºC by 2100 [14]. Still, limiting global warming requires the active and comprehensive commitment of private companies, public institutions, and people.

Even with the current government plans and small successes in the industry, prevailing climate vulnerabilities necessitate multipartite engagement and collaboration in implementation. With the forthcoming LDC graduation, funding earmarked for projects in the least developing countries would no longer be flowing into Bangladesh. It may be time to shift gears towards self-sufficiency in financing green development. Although domestic green financing and debt securities are nascent and require significant bolstering to become functional, heavy private sector involvement is required in both developing viable green ventures and generating its required funding.

Khandaker Raisa Rashed, a Trainee Consultant, and Samiha Anwar, a Business Consultant at LightCastle Partners, have co-authored the write-up. For further clarification, contact here: [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights